Synthetic carbon credit tokens provide derivative exposure to carbon markets (e.g., ICE EUA, voluntary indices) via futures, total return swaps, or oracle-replicated performance, without physical custody or retirement of underlying credits. This delivers operational efficiency (fractionalization, 24/7 liquidity, reduced verification costs) but introduces material counterparty risk (issuer solvency/fulfillment), basis/tracking error risk (deviation from reference index under stress), and fiscal uncertainty (characterization as derivative, security, or intangible property).

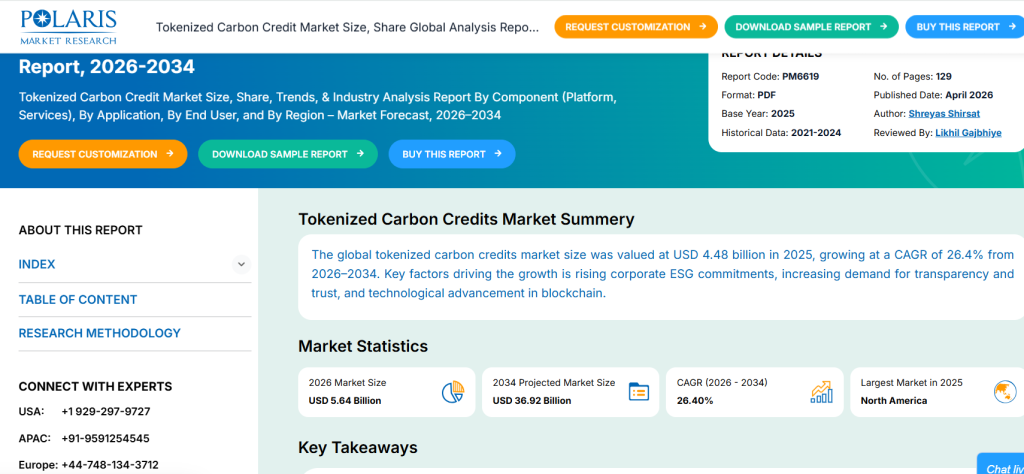

Tokenized/physical carbon markets remain nascent (~$4.5B tokenized credits market 2025 → $37B by 2034 at 26%+ CAGR), dwarfed by broader RWA tokenization (~$27–30B on-chain Q1 2026). Synthetic structures (e.g., via Toucan-style pools, KlimaDAO derivatives, or emerging institutional wrappers) enhance accessibility but amplify risks observed in early bridges (double-counting, quality dilution, “zombie credits”). WEF/BIS tokenization megatrends support adoption; regulatory guardrails (Verra/ACR restrictions, MiCA/FATF) and oracle solutions (Chainlink Proof of Reserve) are critical mitigators.

Synthetics excel in capital efficiency and scalability for portfolio integration (e.g., ESG overlays, hedging) but are not substitutes for high-integrity physical credits. They suit sophisticated investors with robust counterparty due diligence, collateralization, and tax structuring.

Gauging Synthetic Carbon’s Efficiency: Sharpe Ratios, Drawdowns, and Drivers

Synthetic tokens replicate carbon price performance using futures/forwards, Total Return Swaps (TRS), and Oracle-driven synthetics with smart contract mint/burn mechanisms. The value of a synthetic token (St) is mathematically defined as St = Pt × (1 + ϵt) + Ct, where Pt is the reference carbon index price, ϵt represents tracking error, and Ct accounts for collateral adjustments and funding. The tracking error (ϵt) is modeled using a GARCH(1,1) framework combined with a Kalman Filter to capture volatility clustering. Stress periods, characterized by vol spikes and liquidity dry-ups, can significantly inflate tracking error, with historical examples showing basis widening beyond 20-50%. Monte Carlo simulations, employing a quantum-classical hybrid approach under regime constraints and projecting 10,000 paths, estimate a base case annualized Sharpe ratio of approximately 0.8–1.2, indicating an efficiency premium. However, tail risks suggest a 95th percentile drawdown of -45% during counterparty events. Key covariates influencing these simulations include EUA volatility, the US Dollar Index (DXY), energy prices, and regulatory shocks. Further analysis employs the Real Options Valuation framework, conceptualizing synthetic exposure as an American-style call option on carbon abatement. The strike price of this option is determined by the marginal abatement cost curve. This synthetic approach offers a higher convenience yield compared to physical carbon assets, as it avoids the associated custody and verification burdens.

- Advantages: Enhanced efficiency & scalability via DSGE + Factor Decomposition. Operational benefits include no physical custody, registry bridging, or retirement logistics, resulting in estimated 50–80% lower transaction costs. Supports fractional ownership (<1 tCO₂e) and offers 24/7 global access.

- Liquidity & Composability: DeFi integration (lending, yield farming, collateral) boosts velocity, aligning with WEF’s “Tokenization of Everything” narrative.

- Market Impact: Projected tokenized carbon market CAGR of 26%+ (Polaris), with broader RWA growth supporting multi-trillion dollar markets (BIS/IMF).

- Empirical Backing: Toucan/Klima-style structures demonstrated rapid bridging of millions of tonnes, despite quality concerns.

Key risks associated with digital assets, particularly focusing on counterparty, basis, and systemic risks, with an emphasis on applications of graph theory and behavioral economics

Counterparty Credit Risk arises from the issuer’s solvency or oracle failure, where there’s no direct claim on the underlying asset. Mitigation strategies include over-collateralization, Proof of Reserves (as exemplified by Chainlink), and the use of escrow mechanisms.

Basis Risk, also known as tracking error, emerges from the divergence between the digital asset and its underlying physical asset, particularly during market stress. This divergence can be caused by illiquidity, oracle latency, or mismatches in index definitions. A historical example cited is the volatility premium observed between Toucan’s BCT ( a tokenized carbon credit) and spot credit prices.

Systemic Risks encompass a broader range of potential failures within the ecosystem. These include:

-Smart contract bugs: Flaws in the code that could lead to unintended consequences or loss of funds.

-Double-counting: A risk that becomes more significant when bridging between different systems if the bridging mechanism is not robust.

-Additionality/quality dilution: The risk that the value of tokenized assets is diminished by the inclusion of credits that do not meet high additionality standards or are of lower quality, sometimes referred to as “zombie credits.”

–Regulatory bans: The possibility of outright prohibition of these assets or their underlying mechanisms, with Verra and ACR (American Carbon Registry) precedents mentioned as examples of regulatory actions in related fields.

Other analytical approaches to understanding and mitigating these risks: Network/Graph Analysis (using tools like Steelldy Risk Engine 12.4) highlights how the centrality of issuers or oracles can create single points of failure within the network. Conversely, using diversified, multi-oracle setups can effectively reduce contagion risk by spreading reliance across multiple entities. Behavioral Analysis (referencing Steelldy Matrix 2) emphasizes the impact of market sentiment and human psychology. Perceptions of greenwashing can negatively influence asset value, while FOMO (Fear Of Missing Out) during bull markets can amplify mispricing and lead to irrational investment decisions.