Analyse de marché

Analyse de marchéThe Monte Carlo analysis of JPY carry trade unwind uses a Merton Jump-Diffusion model to simulate USD/JPY dynamics over a 90-day horizon, capturing both continuous exchange rate movements and sudden discontinuities from forced position closures. The model incorporates calibrated parameters including a spot rate of 158.5, stressed volatility ranging from 9% to 18%, and jump…

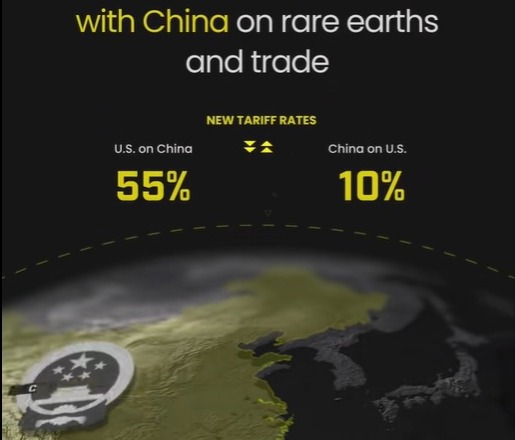

Analysis of the Foreign Exchange Intervention Mechanisms of the Bank of Japan (BOJ) / Ministry of Finance (MoF)

Institutional and fundamental legal framework

Unlike many central banks, the Bank of Japan (BOJ) has no autonomous…

Structured Quantitative Financial Analysis of SpaceX. Consolidated Accounts for Q2 2026 (period ended June 30, 2026)

Revenue decomposition and growth dynamics for Q2 FY26

Consolidated revenue reached 7,814,…

Dr. Copper & Global Recession Risk

Executive Summary

Copper ("Dr. Copper") remains a useful leading indicator of global…

The ETH/BTC ratio currently stands at approximately 0.0292–0.0293

The ETH/BTC ratio currently stands at approximately 0.0292–0.0293 (early August 2026), meaning…

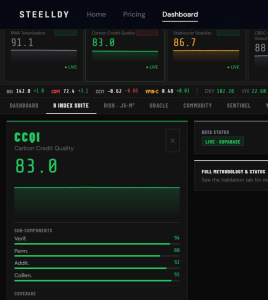

Carbon Credit Market

Carbon Credit Market