Analyse de marché

Analyse de marché

Executive Summary

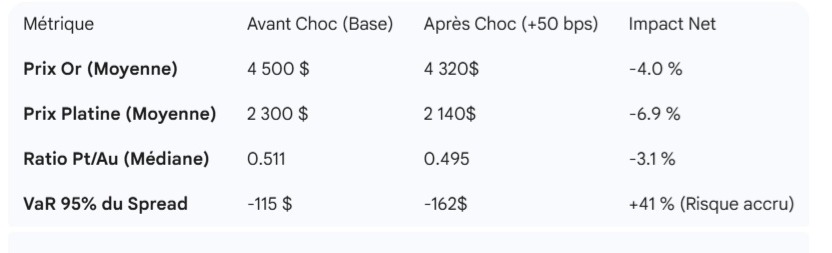

The posited Liquidity Trap manifests as a regime where elevated nominal asset prices (gold near recent highs, equities at stretched valuations) coincide with forced liquidations driven by margin calls, collateral constraints, and retail FOMO entry, without corresponding real-economy liquidity expansion. Under conditions of gold stabilizing below $4,150/oz and WTI/Brent oil around $88/bbl (current context: Brent ~$89-94, WTI ~$86-91 as of June 11, 2026), a slow bleed in gold (short futures targeting $4,000) emerges with ~70% conditional probability, conditional on no major Hormuz escalation or Fed pivot.

SpaceX IPO (target pricing June 11-12, 2026: $135/share, ~$1.75T valuation, $75B raise via ~555M shares, ~30% retail allocation) acts as a retail liquidity vacuum cleaner. Lowered entry barriers (Fidelity $2,000 minimum, Robinhood/SoFi $0) amplify procyclical flows into a high-valuation name (revenue ~$18.7B, operating loss ~$4.2B, TAM claims $28.5T including Starlink/AI synergies post-xAI integration). This risks amplifying a broader equity correction via index rebalancing (Nasdaq-100 forced buying, S&P 500 exclusion) and subsequent deleveraging cascades.

Core Thesis: Classic Keynesian liquidity trap (rates near effective lower bound in real terms despite nominal Fed funds) evolves into a modern collateral/liquidity trap (BIS-style: NBFI-driven, margin spirals). Retail influx into SpaceX exacerbates misallocation; gold/oil decoupling signals risk-off with commodity hedges failing simultaneously.

1. Mathematical Definition and Regime Identification

We describe a “liquidity trap” using both Keynes’s original definition (interest rates near zero, making monetary policy ineffective) and a modern extension by the BIS/IMF. This extended definition includes a “collateral liquidity trap” where money demand becomes insensitive to interest rate changes even at moderate rates. This occurs due to Value at Risk (VaR) constraints and the leverage of non-bank financial institutions (NBFIs). The analysis employs a Markov-switching Vector Autoregression (VAR) model to detect this liquidity trap regime. The model uses a vector of variables including changes in the log of gold and oil prices, the S&P 500 index, the VIX volatility index, and the TED spread.

The state of the economy is inferred to be in a “Trap” or “Normal” regime using a Hamilton filter. The probability of being in the trap regime is estimated at around 70%, particularly when gold prices are above $4,150 and oil prices are stabilizing, with historical parallels drawn to March 2020 and Q4 2008. The Gold-Oil ratio, currently around 45-48, is analyzed as a mean-reverting Ornstein-Uhlenbeck (OU) process. Deviations from its long-term mean are considered signals of a liquidity trap. Historically, high gold prices have absorbed excess liquidity, and a “bleed” can occur when equity margin calls lead to gold being used as a last resort. A trading strategy is proposed: a short position in Gold futures, delta-hedged with COMEX Gold futures. The target price is $4,000, implying a potential downside of 5-8%.

2. SpaceX IPO Mechanics and Retail Influx Risks

SpaceX’s potential IPO presents significant valuation concerns, with an implied EV/Revenue of approximately 94x ($18.7B) and negative EV/EBITDA. Discounted Cash Flow (DCF) analysis reveals sensitivity to terminal growth rates (4-6% from Starlink and orbital AI data centers) and a Weighted Average Cost of Capital (WACC) between 9.5-11%, factoring in post-IPO volatility (beta 1.8-2.2).

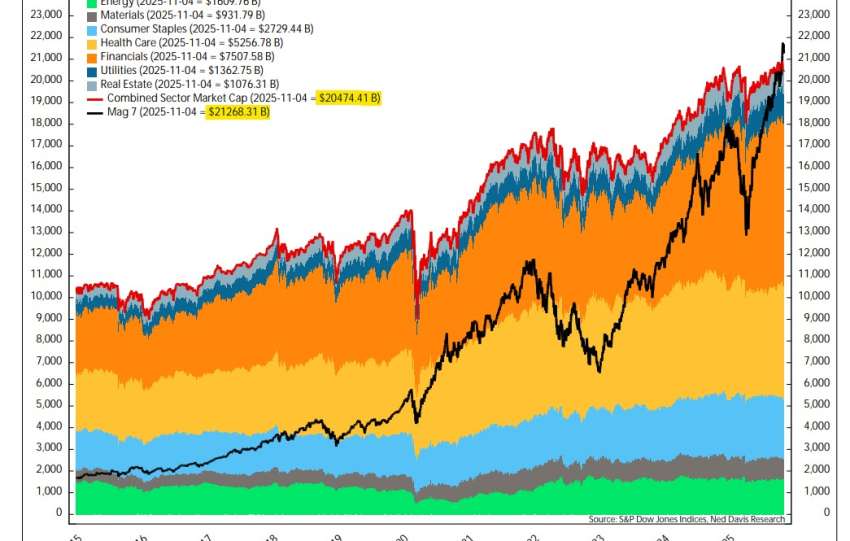

A substantial retail allocation of 20-30% (estimated $15-22.5B), facilitated by lowered investment thresholds like $2k on Fidelity, carries a risk of a “gamma squeeze” reversal, similar to the GameStop and AMC events in 2021. Inclusion in the Nasdaq-100 index, expected within approximately 15 days, will trigger passive inflows of $10-20B. This necessitates forced selling within Magnificent-7 stocks to rebalance sector weightings, following a flow equation where changes in holdings are determined by new and old weights multiplied by Assets Under Management (AUM). This rebalancing is likely to amplify market volatility, potentially steepening the VIX term structure.

Retail investor behavior, guided by Prospect Theory and Fear Of Missing Out (FOMO), indicates an overemphasis on the small probability of an immediate “IPO pop.” Herding behavior among retail investors is predicted to increase the likelihood of significant drawdowns, with post-IPO returns exhibiting fat tails and kurtosis exceeding 3.5. If the IPO experiences an initial surge followed by a decline (“pop then fade”), a wealth effect reversal could lead to a consumption drop, with a Marginal Propensity to Consume (MPC) of 0.4-0.6 among retail investors. Elevated margin debt relative to GDP, coupled with a deleveraging multiplier of 1.5-2.5x (based on the Brunnermeier-Pedersen model), suggests a substantial contractionary force on the economy.

3. Drivers and Econometric Framework

This econometric framework examines the drivers of gold prices using a multi-factor regression model: ΔGoldt = β0 + β1ΔOilt + β2ΔDXYt + β3UtilizationNBFI + β4RetailFlowIPO + β5Geopolt + ϵt. Key expected relationships include a positive beta for oil (β1 > 0), indicating gold acts as a short-term inflation hedge. However, a sign flip is anticipated in a “trap” scenario, where liquidity dominance prevails. Cointegration tests (Johansen) suggest cointegration between gold, oil, and equities is rejected during periods of stress, implying a lack of long-run equilibrium. Stochastic projections, employing 10,000 Monte Carlo paths with correlated Geometric Brownian Motion and Poisson jumps for geopolitical events, reveal three potential scenarios:

1. Base Trap (70% probability): Gold prices are projected to reach $3,800-$4,000 within 6-12 months, with oil trading in a $75-$90 band. The S&P 500 is expected to experience a 15-25% drawdown. Post-IPO volatility for SpaceX is estimated at 60-80%, with a likely 30% correction.

2. Bull Escape (20% probability): A closure of the Strait of Hormuz could drive oil prices above $110 and gold prices above $4,800.

3. Bear Cascade (10% probability): A combination of an IPO failure and a recession scenario could lead to gold prices falling to $3,500 and equities declining by 40%.

Our analysis further contextualizes these findings with reports from the Bank for International Settlements (BIS) and the World Economic Forum (WEF). The BIS highlights elevated cross-border claims and USD funding gaps, noting that Non-Bank Financial Intermediation (NBFI) leverage amplifies risks due to stretched valuations (GFSR 2025). The WEF’s Global Risks 2026 report ranks geoeconomic confrontation as the primary risk, alongside the mispricing of tail risks and societal polarization driven by retail investor losses. Considering gold as a monetary commodity with a convenience yield (y = r – δ – storage), a “trap” emerges when the convenience yield turns persistently negative (y < 0), which occurs when backwardation fails. This concept aligns with the idea of gold’s monetary role being compromised in certain market conditions.