Analyse de marché

Analyse de marchéExecutive Summary

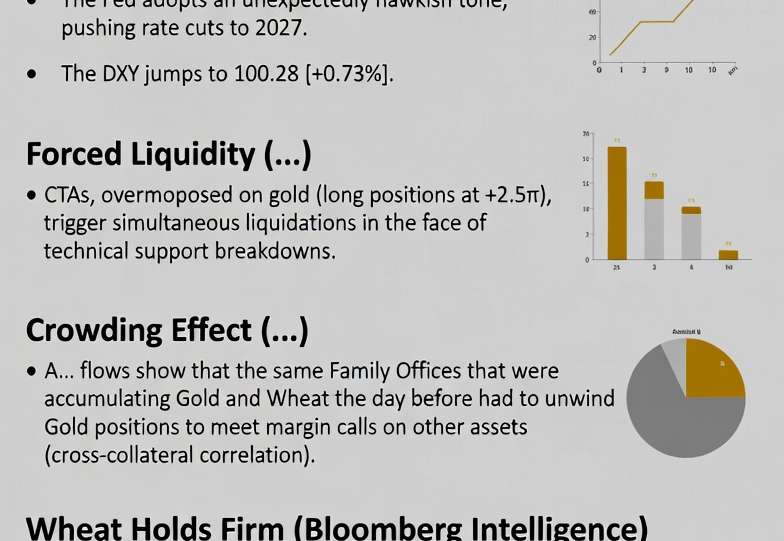

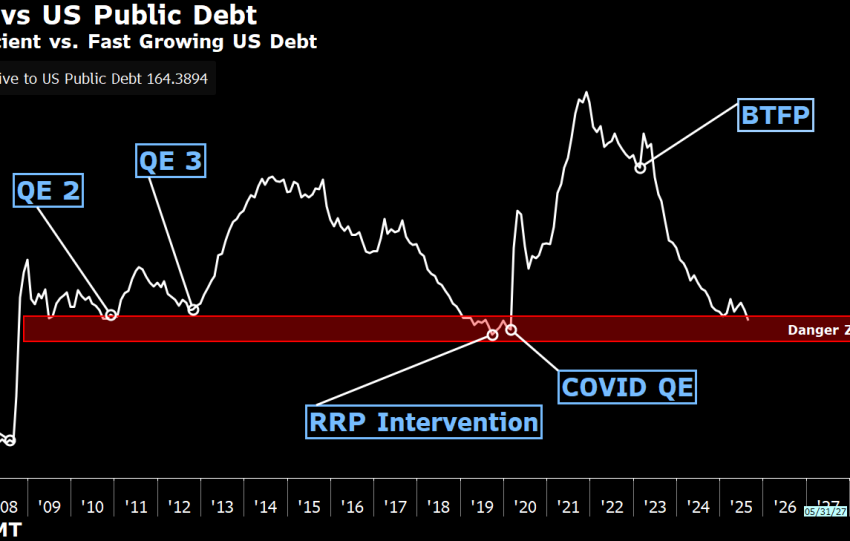

The posited Liquidity Trap manifests as a regime where elevated nominal asset prices (gold near recent highs, equities at stretched valuations) coincide with forced liquidations driven by margin calls, collateral constraints, and retail FOMO entry, without corresponding real-economy liquidity expansion. Under conditions of gold stabilizing below $4,150/oz and WTI/Brent oil around $88/bbl (current…