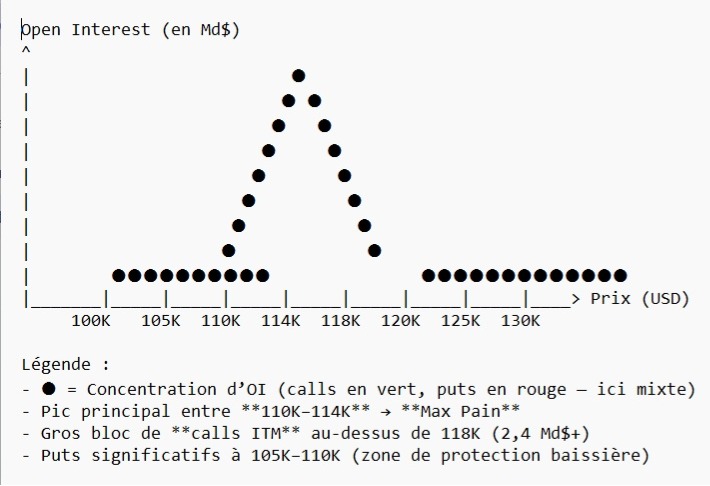

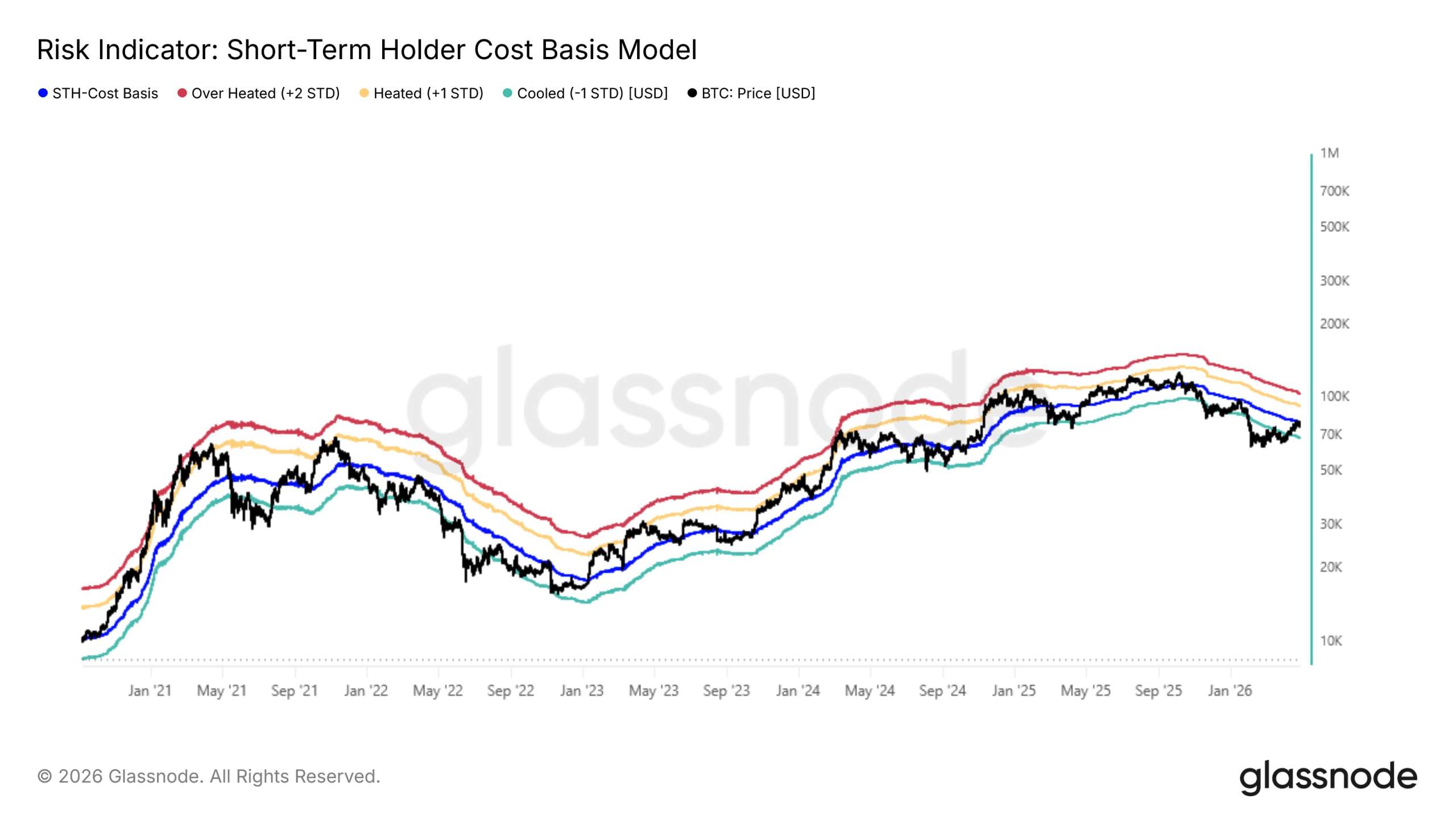

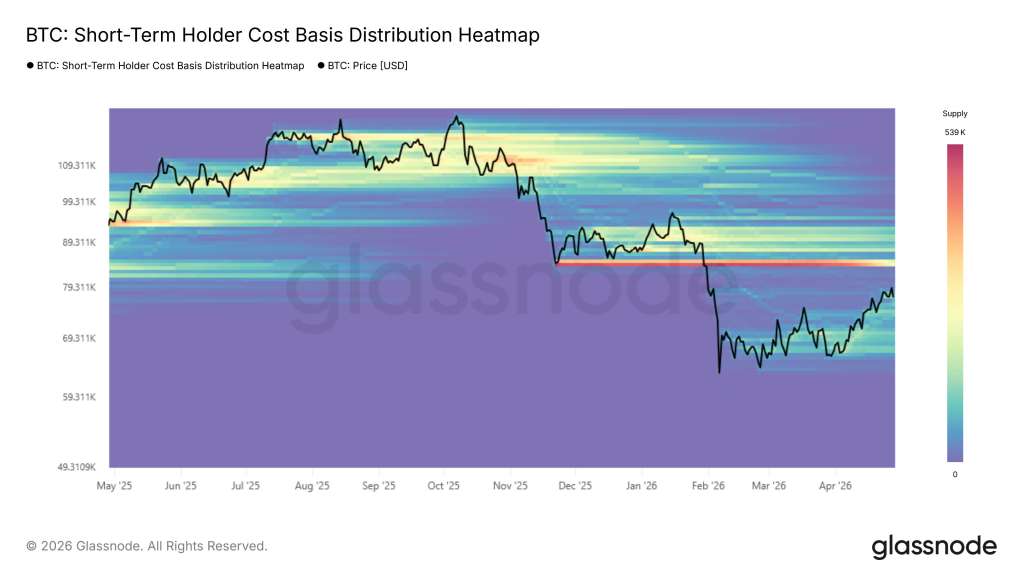

Analysis of Glassnode data as of April 30, 2026, reveals an unprecedented structural compression: Bitcoin is “trapped below market mean,” trading at approximately $76,000, below the True Market Mean (around $81,500) and the STH Cost Basis (around $83,000), in a “Cooled” zone (-1σ).

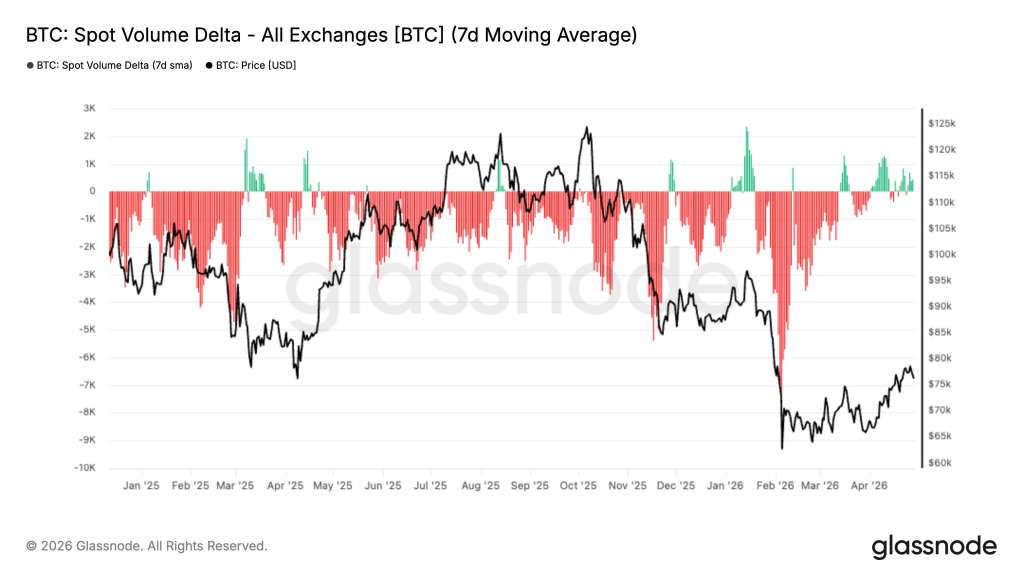

The Spot Volume Delta (7-day MA) indicates a stabilization of net selling flows (easing selling pressure), while the evolution of the 80K call premium exposes an asymmetrical bullish positioning via options.

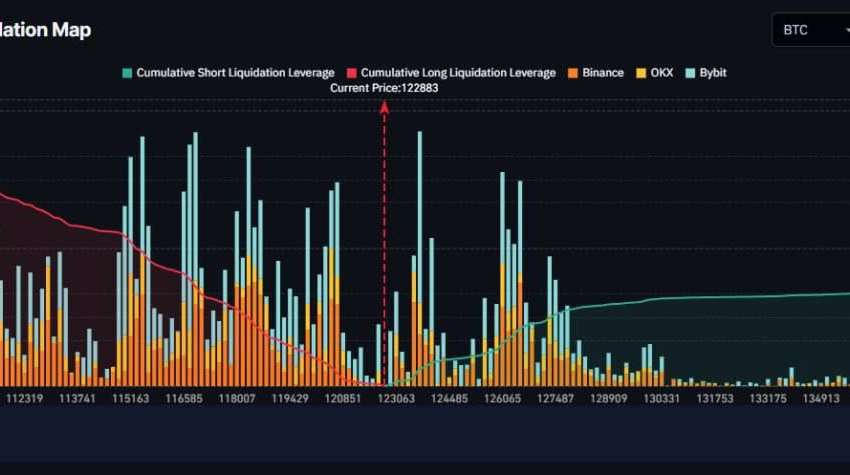

Our model, incorporating new on-chain variables, projects a 42% probability of a technical short squeeze over the T+5 to T+10 day horizon, conditional on a break above $78,200 (confluence of the Hyperliquid $77.5K wall + $80K gamma call).

In the absence of a break, the probability of retesting the $65,000 – $70,000 support rises to 58%. The composite Squeeze Potential Score (SPS), calibrated on funding rate, COT, volume delta, and net 80K call premium, reaches 71.3/100—an “Elevated Squeeze Risk” level (critical threshold: 65). We consider the market to be in a phase of elastic compression: spot demand is low but stabilized, short supply is historically high, and the liquidation map creates a mechanical upward leverage effect if the technical trigger is activated.

Bitcoin is in an elastic compression phase characterized by:

– A trap below the market average (TMP, STH-CB) creating mean-reversion pressure.

– A stabilization of spot flows (Volume Delta) indicating the end of distribution.

– Historically concentrated short positioning (47-day negative funding, Hyperliquid whale, COT LF deleveraging).

– Asymmetrical bullish options positioning (Net Call Premium 80K) setting the stage for a gamma squeeze.

The SPS at 71.3/100 and a 42% probability of a break squeeze represent a high-quality technical setup. However, FOMC risk (35% capitulation) and OPEC+ macro risk (pressure on VIX and liquidity) necessitate strict risk management.

42% on the squeeze timing within 10 days. The trigger remains the break of 78,200 USD.

Whale distribution in cryptocurrency (especially Bitcoin) refers to large holders (“whales” — typically entities with 1,000+ BTC or equivalent massive positions) gradually selling or offloading portions of their holdings, often at higher prices, to smaller buyers like retail investors.

The goal is to exit positions profitably without crashing the market price through a single massive sell order, which would trigger panic, widen spreads, and reduce the average sale price.

Why Whales Distribute Instead of Dumping

A single large market sell can “eat through” the order book, causing a sharp price drop and slippage (selling at worse prices than intended). Whales prefer to sell into strength — when buying pressure from retail or momentum traders is high — so they can offload volume with minimal downward impact. This is often described as “distribution into strength” or “selling the rally.”

In contrast, accumulation happens when whales buy quietly during fear, dips, or low-volume periods when retail is selling or sitting out.

Common Whale Distribution Tactics

Whales use sophisticated, low-impact methods:Gradual/Split Selling (Iceberg or TWAP-style): Break large holdings into smaller chunks sold over time or across multiple wallets/exchanges.

This avoids signaling a major dump and prevents triggering stop-loss cascades or algorithmic reactions. They may sell in the $100k–$1M+ range per tranche rather than millions at once.

Selling into Retail Buying Pressure: During upward moves or “pumps,” retail traders (often smaller orders: $100–$10k) chase momentum and provide liquidity.

Whales (larger orders: $1M+) sell into that demand. This appears in Cumulative Volume Delta (CVD) or order flow tools as divergence: aggressive buying from small players while big players are net sellers.

Creating or Exploiting Momentum:Whales may allow or subtly support short-term pumps (via smaller buys, leverage, or simply holding) to draw in FOMO buyers.

Once euphoria builds and retail provides exit liquidity, they distribute.

Tactics can include coordinated activity across exchanges or using OTC desks for large blocks off public order books.

Order Book Manipulation (Advanced/Riskier): Spoofing: Place large fake buy orders (walls) to create perceived support, encouraging retail buying, then cancel and sell.

Wash trading or layering to fake volume (less common now due to scrutiny).

Stop-loss hunting: Push price to trigger retail stops, creating cheap liquidity, then reverse.

revolut.com

On-Chain and Wallet Strategies:Move funds across multiple addresses to obscure intent.

Deposit gradually to exchanges rather than all at once.

Some whales rotate holdings (e.g., larger whales selling to institutions or ETFs that then accumulate).

insights.glassnode.com

Using Derivatives and Leverage:Hedge or amplify via futures/perpetuals while slowly unwinding spot positions.

This lets them manage risk without immediate spot market impact.

Context from Order Flow (Like the Linked Post)In tools visualizing bid/ask heatmaps, CVD by order size, and liquidity clusters:Retail aggression (small orders) often shows as strong buying on green candles or bounces.

Whale distribution shows as larger red (sell) delta even as price holds or rises, because big players are hitting bids without fully depleting visible support.

Visible bid liquidity around $76k–$80k can act as a “wall” that whales sell against, effectively transferring coins from strong hands (whales) to weaker hands (retail chasing the move).

This dynamic is classic in market cycles: Whales accumulate in capitulation/fear → price recovers → retail buys euphoria → whales distribute → potential exhaustion and correction.Detection and CaveatsOn-chain signals: Rising exchange inflows from large addresses, shifts in whale balance subdivisions (e.g., 1k–10k BTC group vs. bigger ones), or declining exchange reserves alongside whale outflows.

Order flow/CVD divergence: Smaller buyers dominant on upsides; larger sellers on volume.

Not every large sell is malicious distribution — it could be rebalancing, collateral moves, or institutional needs.

Whales aren’t always coordinated; “whale wars” or rotations (e.g., old whales to new institutional buyers) occur.

Distribution doesn’t guarantee an immediate crash — markets can stay elevated while supply is absorbed, especially with strong inflows (ETFs, corporates). However, sustained whale selling into retail strength often precedes periods of weakness or consolidation once buying pressure exhausts.Retail traders watch these signals (via Glassnode, Nansen, on-chain dashboards, or order flow tools) to avoid “buying the top” from smart money exits. Always combine with broader context like macro, ETF flows, and sentiment. This is market dynamics, not guaranteed outcomes — trade responsibly.