Analyse de marché

Analyse de marché

The U.S. labor market – a facade of stability

https://www.steelldy-indices.com

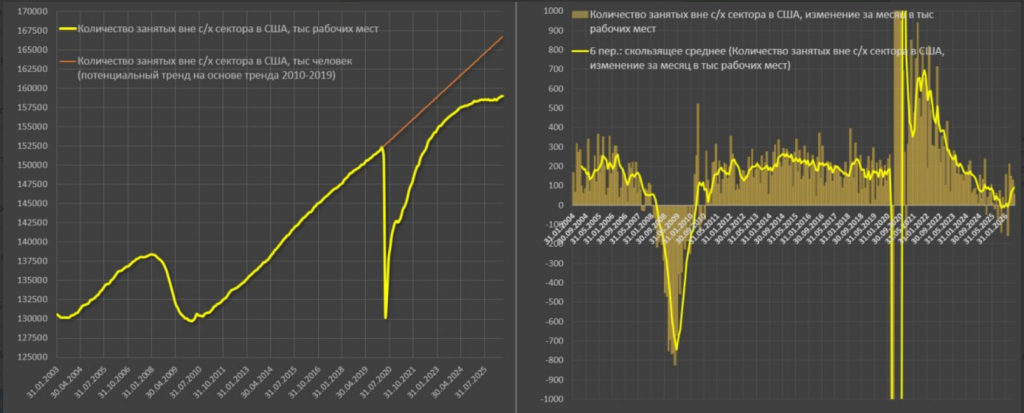

To grasp the scale of the problem, between February 2025 (Trump taking office) and June 2026, the average monthly job creation in the U.S. was only 42,000 (4.5 times below normal), with the private sector adding 53,000 jobs and the public sector shedding an average of 11,000 per month. However, within the private sector, healthcare and social assistance generated 56,000 jobs, meaning a loss of 3,000 jobs per month excluding healthcare, modest by the scale of the U.S. economy, but the break in trend is significant, as the trend in the private sector excluding healthcare was around 128,000 jobs per month between 2017 and 2019.

Consequently, the economy has missed over 2.2 million private-sector jobs in the last 17 months. Thus, any trend analysis boils down to a structural observation: healthcare dominates entirely, while the rest of the economy is already on a medium-term downward trajectory. To be fair, the break in the upward trend occurred not in February 2025, but in November 2023. Between November 2023 and January 2025, average monthly growth in the private sector excluding healthcare was… zero! So it’s not 17 months, but 32 months of stagnation with a slight downward trend, a loss of 37,000 jobs in this group, or about 1,000 per month. Momentum was largely lost in March 2023 (between March and October 2023, only 48,000 jobs per month were created in the private sector excluding healthcare). Thus, from March 2023 to June 2026 (40 months), only 349,000 jobs were created, or 9,000 per month. For comparison, average monthly growth was 128,000 in 2017-2019 and 155,000 in 2011-2019, in absolute figures without adjustment for population growth.

This means that if the economy had created jobs at the 2017-2019 pace from March 2023, there would have been 5.1 million more, and at the 2011-2019 pace, 6.2 million more. In reality, it would be even higher, given demographic trends in the U.S.

As for trends, taking March 2023 as the start of the “failure,” with an intensified negative trend since November 2023, the cumulative tally is as follows:

• Professional and business services: -330,000 jobs

• Manufacturing: -300,000 • IT and telecommunications: -274,000

• Retail trade: -143,000

• Finance and insurance: -48,000

• Wholesale trade: -32,000

• Mining: -26,000.

In total, seven sectors shed 1,153,000 jobs, currently representing 69.1 million of the 135.6 million private-sector jobs, meaning 51% of the economy is in contraction (weighted by job count). This is even more significant in terms of compensation, as the “fattest” sectors (professional services, IT, finance) are hit hardest.

This is the second key conclusion: the highest-paying jobs are in decline. In June, 57,000 jobs were created. May data were revised downward from 172,000 to 129,000, and April from 214,000 to 148,000, a loss of nearly 100,000 jobs. In the first six months of 2026, 552,000 jobs were created, including:

• Private sector: +530,000

• Public sector: +22,000

In the private sector:

• Healthcare and social assistance: +319,000

• Professional and business services: +135,000

• Construction: +59,000

• Transportation and logistics: +48,000

• Retail trade: +46,000

• Educational services: +27,000 Cuts:

• Financial sector: -82,000

• Information sector: -68,000

• Hospitality and food services: -21,000

Thus, healthcare provided about 60% of private-sector job growth in the first half of 2026. No need to go into details. Each year, statistics are revised, and we’ve grown accustomed to “burning” up to a million jobs at once, so monthly gains of 80,000 to 100,000 can turn into “nothing” in the next revision.

Slowing U.S. Economy and Falling Inflation Pressure Could Propel Gold to $4,200

The June U.S. employment data suggests a potential turning point for the gold market. While inflation remains a threat, the Federal Reserve was reminded of its dual mandate as the labor market slowed, with only 57,000 jobs added against an expected 114,000. This weaker data could provide short-term support for gold, which rose 2% above $4,100 per ounce, breaking an eight-year losing streak. Spot gold traded at $4,108, up 0.51% from the previous week.

The unemployment rate fell to 4.2% but reflected a declining labor force participation rate, indicating economic instability. Analysts suggest the Fed may not raise rates by year-end, which would benefit gold as investors recognize this. David Morrison of Trade Nation sees potential for a gold bottom, noting the metal held support around $3,950-3,960 after dipping below $4,000.

The four-month correction has left gold oversold, and the employment report reinforces hopes for a significant rebound. Markets now price a 25% chance of unchanged rates through 2023, with some analysts believing the Fed’s hawkish stance is overestimated.

Lukman Otunuga of FXTM notes that gold found support from Fed Chair Kevin Warsh’s comments, emphasizing commitment to price stability but acknowledging reduced inflation risks. Geopolitical tensions easing, lower oil prices, and reduced global inflation pressure could further support gold, potentially pushing it toward $4,200 and the 200-day moving average. However, not all analysts are convinced the bearish correction is over.

Fawad Razaqzada of FOREX.com warns that gold recovery may remain elusive due to the strong U.S. dollar, which poses a short-term threat. Ole Hansen of Saxo Bank highlights the need for further dollar weakness and lower bond yields for a technical breakout above $4,215.

With limited economic data next week, gold will remain sensitive to geopolitical news and oil prices. Morrison notes that the main risk is oil prices rebounding from oversold levels, reigniting inflation fears, but this may be temporary. Overall, while fundamentals suggest pressure on oil due to slowing demand and ample supply, a sustained drop in oil could help keep inflation expectations anchored.