The impact of the Pillar Two international tax regime (OECD) on the valuation and structuring of tokenized carbon credit (TCC) investments, particularly in France.

(A) Structural effect of Pillar Two on the taxation of TCCs

¤ Pillar Two imposes a minimum effective rate of 15% on the profits of multinational corporations, neutralizing tax optimization strategies based on lower rates. In France, the introduction of the QDMTT (Qualified Domestic Minimum Top-up Tax) primarily captures the top-up tax, limiting the erosion of the tax base by other jurisdictions.

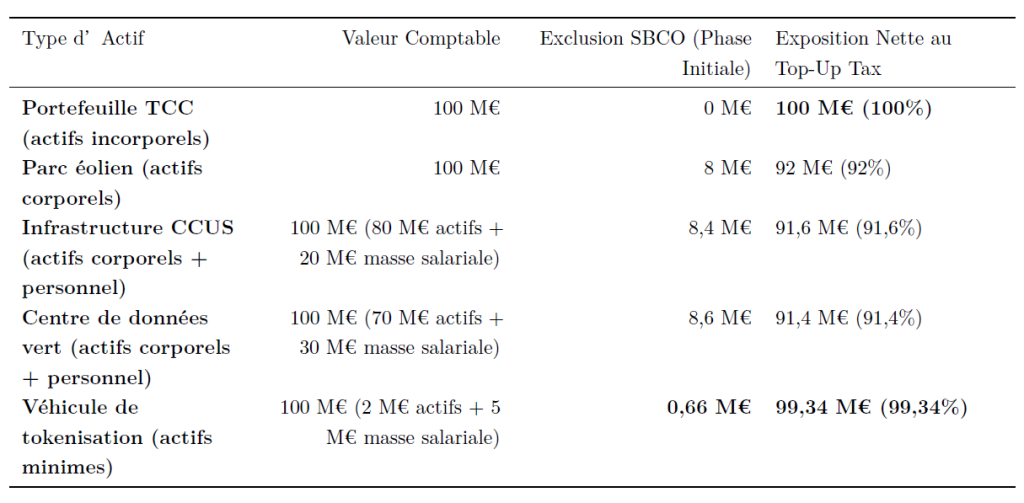

¤ Tokenized carbon credits, considered intangible assets, do not benefit from the Substance-Based Carve-Out (SBCO), exposing their entire return to the top-up tax if the effective tax rate is below 15%.

(B) Penalization of models with high intangible asset intensity

¤ CCAP portfolios held by investment vehicles with low operational substance are particularly penalized because they cannot reduce the top-up tax base via the SBCO. This creates a ‘substance trap’ for tokenized carbon investments.

¤ Example: A €100M CCAP portfolio with no tangible assets will see 100% of its return exposed to the top-up tax, whereas a similar industrial portfolio will benefit from a base reduction.

(C) Reduced effectiveness of non-refundable tax credits

¤ Non-refundable tax credits reduce the effective tax rate but can trigger the top-up tax if this rate falls below 15%, partially or totally cancelling the initial tax benefit. Value erosion can reach 40 to 70% depending on the configurations.

¤ Conversely, qualified refundable tax credits (QRTC) are more effective because they do not negatively affect the calculation of the effective tax rate.

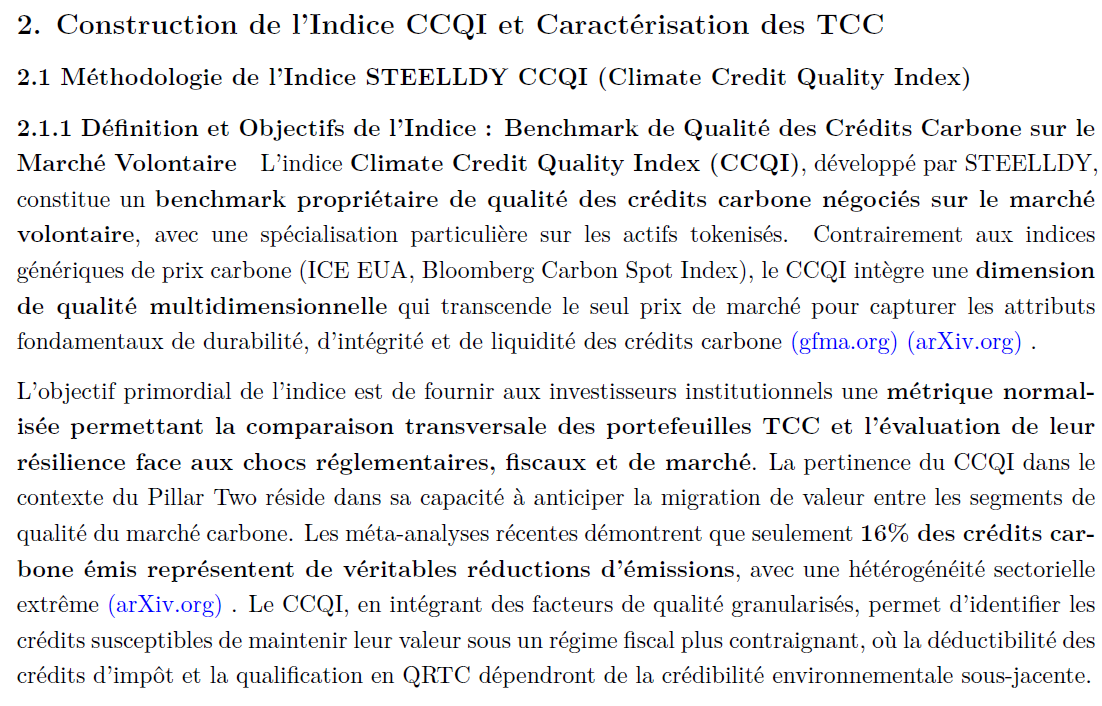

(D) Importance of Carbon Credit Quality (CCQI)

¤ High-quality carbon credits (high CCQI, CCP certified) benefit from a quality premium that acts as a buffer against tax erosion. Simulations show that only high-quality portfolios maintain a positive net return after the application of Pillar Two.

¤ Example: A portfolio with CCQI > 75 shows a net annualized return of 8.2% compared to 2.1% for a low-quality portfolio.

(E) Enhanced correlation between credit quality and tax risk-adjusted performance

¤ During a tax shock period (increase in top-up tax), the correlation between the CCQI STEELLDY index and the tax risk-adjusted performance of SMEs increases, making the CCQI a key indicator for risk management and portfolio selection.

(F) Necessity of proactive structuring

¤ We recommend proactive structuring of investments to maximize the CTRA qualification of tax incentives, integrate more tangible assets, and prioritize high-quality carbon credits to preserve net after-tax value.

¤ Simulations show that tax neutrality can erode up to 57% of a portfolio’s value in an extreme stress scenario, highlighting the importance of regulatory and tax foresight.

(G) Transitional arbitration window

¤ There is a temporary fiscal arbitration window in jurisdictions with deferred Pillar Two implementation, but this window will close quickly as regulatory convergence occurs.

In summary, we conclude that Pillar Two radically transforms the taxation of tokenized carbon investments in France, penalizing models with high intangible asset intensity and making the quality of carbon credits crucial for preserving net performance. Tax structuring and rigorous asset selection become essential levers for limiting value erosion caused by international tax neutralization.