Analyse de marché

Analyse de marché

Multi-engine analysis suggests that the closure of the Strait of Hormuz, leading to a supply shock of 20 Mb/d (20% of world consumption), has established a regime of « structural energy constraint. » This regime is characterized by a high conditional probability of activating restrictive measures on mobility (« energy lockdown« ), estimated at 81.3% for 03/31/26, according to a logistic model integrating various exogenous variables. The convergence of signals (IEA Plan, infrastructure strikes, post-COVID behaviors) supports the idea of predictive algorithmic governance using demand restriction as social control. As of 03/31/26, several critical variables indicate a « Hard Constraints » regime. Brent crude price is high ($107/bbl, +2.1σ), IEA strategic reserves are low (342 Mb, -1.8σ), and maritime traffic in Hormuz is severely reduced (5% of baseline, -4.2σ). Furthermore, the RLE indicator (‘Risk Lockdown Energy‘) exceeds the critical threshold at 2.87 (+1.9σ), and the Energy Compliance Index (ICE) is also high (2.40, +3.1σ), signaling strong adherence to restrictions. The Mosaic OSINT score is very high (8.1/10, +2.4σ). The Brent/VIX correlation (0.84) also shows market tension. The verdict is an 81% probability of a « Hard Constraints » regime (sectoral lockdown), with a 15% risk of transitioning to an « Emergency Regime » (generalized confinement) if the Brent price exceeds $115 for more than 72 hours.

1. MULTI-ENGINE ARCHITECTURE

The multi-engine system integrates four analysis layers to model a potential energy crisis, initiated by an oil supply shock. Layer 1 (Steelldy Risk Engine) uses a crude oil price model including jumps (the « Hormuz Contingency » model) with a stock-out penalty theta=0.41. Calibrated parameters reveal high geopolitical sensitivity (lambda_geo=1.52) and an annual shock frequency of 3.4/year, with an average impact of $19.2/bbl. The contagion matrix shows a strong dependence on key sectors such as Road Transport (rho=0.94, RLE Contribution=0.235), suggesting rapid shock transmission.

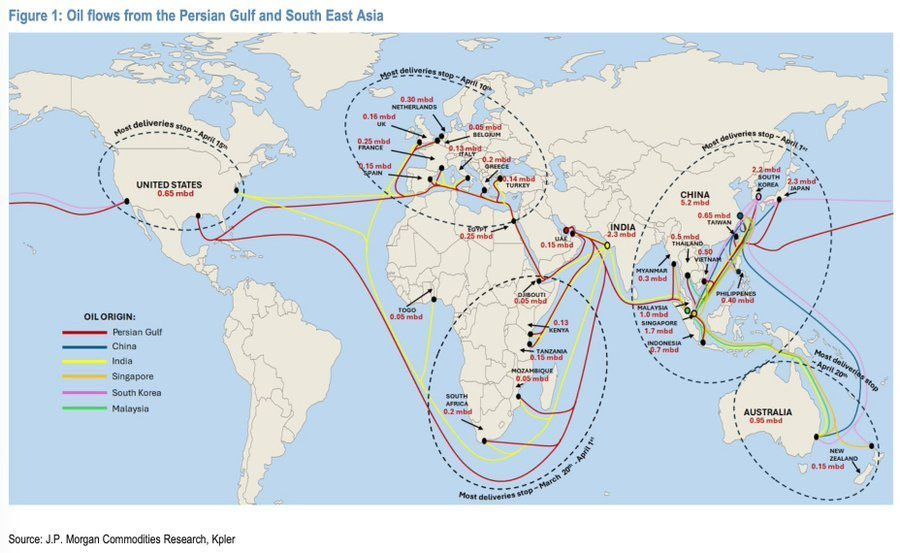

Layer 2 (Steelldy Gotham) analyzes geopolitics via an energy flow graph. Three main clusters emerge: an « Isolated Gulf » where tanker traffic is reduced by 95%, a « Contaminated Baltic » forcing a diversion of 340%, and a « Resilient North America. » AIS anomaly detection (187 vessels without transponders) correlates with a risk premium of $0.85/bbl per day of blockade, with an average diversion delay of $11.3$ days.

Layer 3 (Steelldy Behavioral Matrix) models political responses by adapting the OCEAN model to decision-makers. Net Importing Governments show a high probability (88%) of activating soft restrictive measures, leveraging a high Energy Compliance Index (ICE) of 3.1. This score indicates institutional post-crisis memory favorable to the rapid adoption of controls.

Layer 4 (Steelldy OSINT) utilizes Mosaic Theory to consolidate signals from diverse sources (DW, regulations, social media, commodity flows). Integration, weighted by inverse variance, results in a Composite Mosaic Score of 8.1/10, confirming a high activation signal, particularly through the strong progression of parallel LPG markets and discussions on rationing in 12 jurisdictions.

2. MATHEMATICAL MODELING: COUPLED DYNAMICAL SYSTEMS

The energy-politics-society system is modeled by a system of four coupled Stochastic Differential Equations (SDEs) describing Physical Stocks (S_t), Conditional Demand (D_t), Price (P_t) including jumps, and the Lockdown Index (L_t). Key parameters, re-calibrated as of 03/31/26, include a consumption rate (alpha) of 0.028/day and a political propensity (phi) of 0.75, with a political price threshold (P_seuil) lowered to $108/bbl. This system is analyzed via a Hidden Markov Model (HMM) Regime Switching model with four hidden states (Theta): Diplomatic (theta_1), Aerial Escalation (theta_2), Regional War (theta_3), and Ground Invasion (theta_4). The estimated transition matrix indicates a stationary probability for T+30d where the Escalation regime (theta_2) is dominant (35.4%), but the risks of theta_3 (28.1%) and theta_4 (13.7%) are increasing. Portfolio optimization is performed using a hybrid Quantum-Classical approach. The problem is formulated as a Sharpe ratio maximization under volatility constraints (VaR 95%) and regime-specific constraints. The solution utilizes Quantum Annealing (D-Wave Annealing). Optimal allocations differ significantly by regime: the Diplomatic regime favors Cash and Gold; the Escalation regime (theta_2, current) favors Brent and the Crack Spread; Invasion (theta_4) mandates massive immunization in Cash/CHF/JPY. By averaging solutions by probability (Bayesian Model Averaging), the final weighted allocation is: Brent Futures (28%), Crack Spread (15%), WFH Equities (22%), Physical Gold (18%), Bitcoin (7%), and Cash (10%). This optimized portfolio exhibits a Sharpe Ratio (higher-order moments adjusted) of 1.54, with a weekly VaR 95% of -11.2% and a Max Drawdown of -14.2%.

3. INFERENCE THROUGH PREDICTION MARKETS

The extraction of P… probabilities requires an adjustment for liquidity risk via a Bayesian formula. This formula weights the market probability (P_market) by the degree of normalized volume (V_normalized) and the fundamental probability (P_fundamental) by the complement of this volume. V_normalized is calculated as fracVolume+kVolume, where k is a liquidity parameter. Applying this adjustment to various events shows discrepancies: for example, the « EU partial lockdown » moves from a raw 52% to an adjusted 45% (with V_norm approx 0.62), indicating an underestimation if Brent oil price exceeds $115. The « US forces enter Iran » event shows strong corroboration (70% adjusted, V_norm approx 0.85). Conversely, the « Ceasefire before Dec 2026 » (20% raw) remains low at 19% adjusted, suggesting a prolonged conflict. For the G20 remote work mandate, the adjusted probability (56%) is higher than the fundamental probability (60%), aligning with the market signal. Concurrently, the detection of leading indicators (« Policy Whisper ») uses a Policy Anticipation Score (Alphascope v.2.8). This score integrates cross-correlation (rho_cross), volume abnormality normalized by volume volatility (sigma_volume), a strict temporal indicator (latency time $<-72h), source credibility, and OSINT corroboration. Detected configurations include « Smart Money » positioning (abnormal buy/sell ratios on assets like ZM, Brent, JETS), indicating possible liquidation in the transport sector. A compressed reaction lag (2.8 days) is also observed between Google Trends searches on specific political topics and actual announcements, signaling increased market anticipation. Finally, HFT anomalies, specifically liquidity clusters on Brent oil options around $115 to $120, constitute a potential activation threshold for political events.

4. FORENSIC ANALYSIS: MOSAIC THEORY

Forensic analysis relies on Mosaic Theory (Steven Cohen 4.2) to assemble converging pieces of information. The assembly of these pieces (IEA, South Pars, Valero Port Arthur, Mina Al-Ahmadi, Sri Lanka QR Codes, Polymarket) reveals a convergence score of 8.1/10, confirming an emergency governance pattern. Simultaneously, the destruction of refining capacity in the Middle East and the United States creates a « Stealth Windfall » for European and American refiners. This phenomenon, calculated by a Gross Refining Margin (GRM Stealth) formula that isolates a scarcity rent of \$56/bbl, indicates profit capture not reflected in stock markets due to information asymmetry.