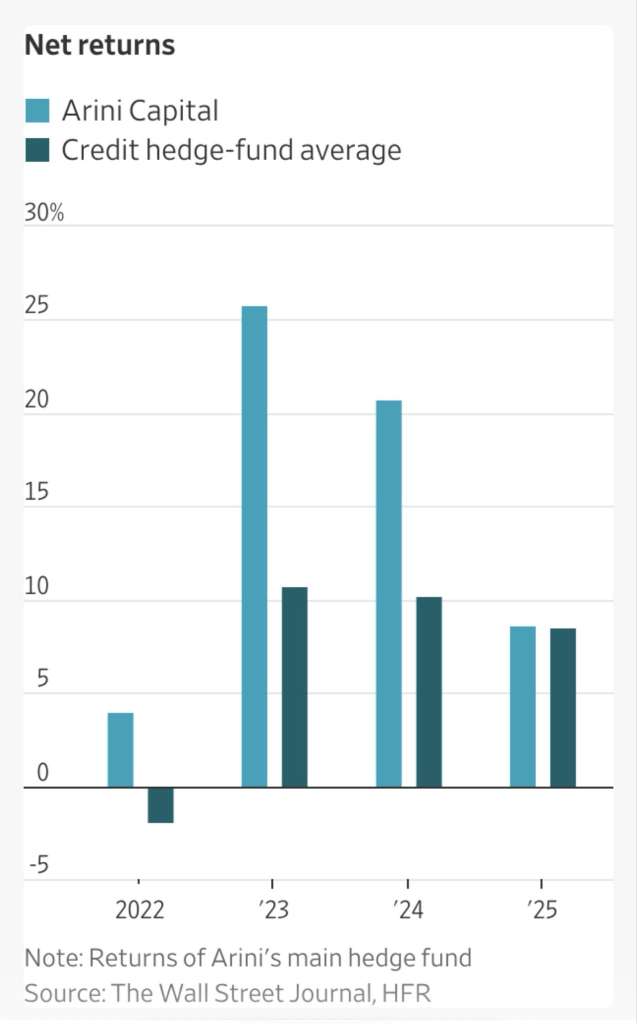

Hamza Lemssouguer‘s Arini Capital fund, launched in 2022 with $1.3 billion and reaching $20 billion in assets under management, is highlighted for its focus on European distressed debt and high-yield credit refinancing for companies like Altice. Arini closed its flagship fund at $4 billion to maintain performance and is expanding into CLOs and private credit. Its highly leveraged strategy has generated high returns (~25% in 2023, ~20% in 2024), outperforming the average for credit funds, but raises concerns about its vulnerability should bets on debt reverse. Approximately 60% of the funds come from North American investors.

The major concern regarding Arini Capital, despite its excellent performance (+25% in 2023, +20% in 2024), lies in its intensive use of leverage in its strategy focused on European distressed and high-yield debt. This approach, utilizing techniques like Total Return Swaps to amplify exposure (often 3x to 8x) on concentrated bets (examples cited: Altice, Very Group), is extremely vulnerable to a market downturn. If credit spreads widen or defaults increase, the mechanical amplification of losses rapidly erodes the Net Asset Value (NAV). The strategy faces several risks specific to the European market: the low liquidity of distressed assets, which can make margin calls potentially dangerous and may force fire sales. Furthermore, the concentration of positions in the same companies exposes the fund to correlation risk. About 60% of capital comes from North American investors, who can redeem their funds quickly (quarterly redemptions), increasing liquidity pressure on a fund whose capacity is already limited ($4 billion for the main fund).

In essence, the exceptional performance relies on a strong directional bet dependent on a favorable credit environment. Critics argue that if credit risk materializes, the leverage transforms a manageable decline into a swift catastrophe, a typical situation for heavily committed credit strategies.

Arini Capital has generated remarkable alpha (25% in 2023, 20% in 2024) by exploiting the European “distress premium” through extreme concentration and high structural leverage (4x to 8x via TRS/Repo).

Our analysis, however, reveals negative asymmetrical convexity: the strategy depends on the continuity of liquidity and the success of restructurings. An exogenous shock (rates, supply chain, systemic default) combined with [concentration, leverage, Illiquidity] exposes the NAV to an extinction risk far higher than peers. This alpha is in reality a sale of options on volatility and liquidity.

Risk modeling shows that leverage L strongly amplifies the variance of returns on “distressed” assets, whose distribution follows a heavy-tailed law. A 10% drop in the asset with L=5 causes a 50% loss of capital, triggering “Gate” and “Side Pocket” clauses.

The Altice case study shows that debt complexity and legal “drop-down” risk can impose a severe “haircut“, multiplied by the 5x leverage from TRS, resulting in a 50% loss on the trade for a 10-point price decline.

For Very Group (private debt), the “MtoM” valuation (Level 3) is illusory; a closing of the exit market would cause the real value to plummet. If Repo leverage is applied to this illiquid debt, a credit downgrade drains the fund’s liquidity.

Finally, 60% of capital from US investors subject to strict VaR makes the fund vulnerable to redemptions. A 5% drop in NAV could trigger Redemptions that the fund must stop using “Gates” and “Side Pockets,” destroying its reputation and freezing capital. The strategy is a sale of asymmetry: capped upside potential, downside potential amplified by leverage. Illiquidity serves as hidden leverage. The failure of Arini (€20 billion) would lead to a systemic feedback loop on European credit.

Arini Capital deploys a concentrated, high-leverage strategy, combining “distressed,” “high-yield,” and “capital solutions” exposures, as illustrated by its key positions in Altice and Very Group.

In the case of Very Group, the British online retail platform, Arini acted as a private credit lender. In April 2025, Arini acquired £598 million in privately issued senior secured notes, fully refinancing existing debt due in August 2026. This new debt matures in August 2027, with an extension option until 2030, conditional on deleveraging. This financing aims to solidify the balance sheet before a potential sale. The position is senior secured (asset-backed), but it remains exposed to e-commerce sector risks and the failure to meet debt reduction targets. Fitch also upgraded the group’s credit rating following this transaction.

Regarding Altice (Patrick Drahi’s telecom group), Arini’s exposure is typical of distressed bond trading. Arini is a central player in the creditor committees for Altice France and Altice International, holding secured and unsecured bonds. Faced with complex restructuring maneuvers and asset “drop-downs” by Patrick Drahi, Arini actively participated in negotiations to amend debt terms. For Altice France, the debt was reduced (from €24 billion to €15.5 billion), creditors receiving about 45% of the equity, while unsecured creditors suffered significant write-downs. On Altice International, Arini helped organize a cooperation agreement among senior creditors to counter asset transfers. These two investments are characterized by high concentration and the frequent use of leverage (TRS or repo), allowing for significant gains in a favorable scenario, but exposing the fund to an increased risk of amplified losses (margin calls in case of market stress or restructuring failures), leading some observers to describe this strategy as potentially “prone to backfiring” during systemic shocks or payment defaults.

Here is the highest level of granularity publicly available (sources: Bloomberg, Octus, CreditSights, Cbonds, TISE, Reuters, Ropes & Gray – data up to April 2026). Arini never discloses the exact size of its positions or leverage per ISIN, but it is known that Arini + Attestor (and a small group) held > €1.55 Bn of secured + unsecured cross-holdings in Altice France as of March 2024, and that Arini is part of the secured SteerCo on Altice International (85% of senior creditors covered by a cooperation agreement).

1. Altice France – Pre- and post-restructuring positions (October 2025)

Historic Restructuring: Debt reduced from ~€24 Bn to €15.5 Bn (elimination of > €8 Bn). Creditors obtained ~45% of the equity (of which ~31% for secured creditors); Drahi retains 55% with no cash injection. Arini/Attestor were leaders of the creditors’ committee (along with Houlihan Lokey + Milbank/Gibson Dunn).

Main ISINs involved (pre-restructuring, 2024):

XS2053846262 → Altice France S.A. 3.375% 19/28 (senior secured)

USF0270BAB83 → Altice France (SFR Group) 6.875% 10/15/2030 USD (senior)

XS3161792075 → 7.25% 11/01/2029 EUR (new post-restructuring, Reg S)

XS3161792406 → 4.75% 10/15/2030 EUR (new, Reg S, outstanding amount ~€770 M)

USF0270BAE23 / US02090DAE85 → Other senior secured notes (Reg S / 144A) listed on TISE USL0183LAA72 → 10% / 9.125% 01/15/2033 USD (new post-restructuring)

Historical Prices (representative examples from the stressed period 2024-2025):

¤Mid-2025: bonds such as Altice Finco 4.75% Jan 2028 (XS1577952440) traded at 31-33 cents (very distressed). ¤Before the drop-down / restructuring announcement (March 2024): prices already depressed (very wide spreads). ¤Post-restructuring (Oct. 2025): new bonds stabilized higher due to deleveraging (but remain high-yield).

2. Altice International – Current position (Dec. 2025 – ongoing)

Arini is one of the main secured creditors on the SteerCo (along with Sona, PGIM, Invesco, BlackRock, King Street). They reacted immediately to the massive drop-down of assets (Portugal + Caribbean = ~80% of EBITDA moved out of the restricted group).

Main exposed tranches (no exhaustive public ISINs, but Octus details):

| Maturity | Amount | Coupon | Post-drop-down Price (Dec. 1, 2025) | Comment |

|---|---|---|---|---|

| 2027 | ~€1,1 Md + $375 M | Variable (EURIBOR+5 %) / 9,625 % | ~77 | Senior secured |

| 2028 | €1,1 Md + $1,2 Md | 3 % / 5 % | Mid-60s (baisse 6-8 pts) | Senior secured |

| 2029 | $2,05 Md + €805 M | 5,75 % / 4,25 % | Mid-60s (baisse 6-8 pts) | Senior secured |

| 2028 | €675 M | 4,75 % | 16-21 (baisse >14 pts) | Subordinated (GoldenTree principal holder) |

These prices reflect the shock of the drop-down (transferred assets and new senior debt priming the bonds). Arini and the SteerCo engaged Gibson Dunn + Houlihan to defend the covenants.

3. Arini vs Attestor Capital

Comparison On Altice France (2024-2025): Direct partners. Both funds constituted the hard core of the committee (> €1.55 Bn cross-holdings), appointed the same advisers, and negotiated together. Identical result: equity stake and deleveraging. Attestor is sometimes cited as a co-leader with Arini.

On Altice International: Arini is explicitly in the secured SteerCo (85%). Attestor is not listed in the latest group (Dec. 2025), but the two funds often chase the same European distressed deals.

Style & risk: Very close (London-based credit hedge funds, high leverage, activist approach). Arini has been more focused on “capital solutions / scalable private credit” since 2025 (CLOs, direct lending like Very). Attestor remains a purer “special sits” player. Both have outperformed on Altice thanks to the restructurings, but both are exposed to the same “Drahi playbook” risk (drop-down + haircuts).

Key difference: Arini closed its flagship fund at $4 Bn to preserve performance; Attestor is larger and more diversified.

4. Very Group (quick reminder – fewer public ISINs)

Arini purchased £598 M of senior secured notes (private placement, April 2025 maturity) to refinance £575 M due August 2026.

Maturity: August 2027 + possible 3-year extension if deleveraging + rating upgrade.

Company ISIN (not Arini’s) known: XS3045495218 (9.75% Senior Secured Notes due 2030, £553 M outstanding). The Arini issuance is private – no public ISIN available. Fitch upgraded the rating to B- after the deal.

Link with the leverage/vulnerability concern: These concentrated positions (Altice in particular) are typically amplified by TRS / repo (estimated leverage of 3-8x). A 5-8 point drop, as seen in Dec. 2025 on Altice Intel, results in highly amplified losses + risk of margin calls / fire sales if North American redemptions occur. This is exactly the “prone to backfiring” mentioned by the WSJ.