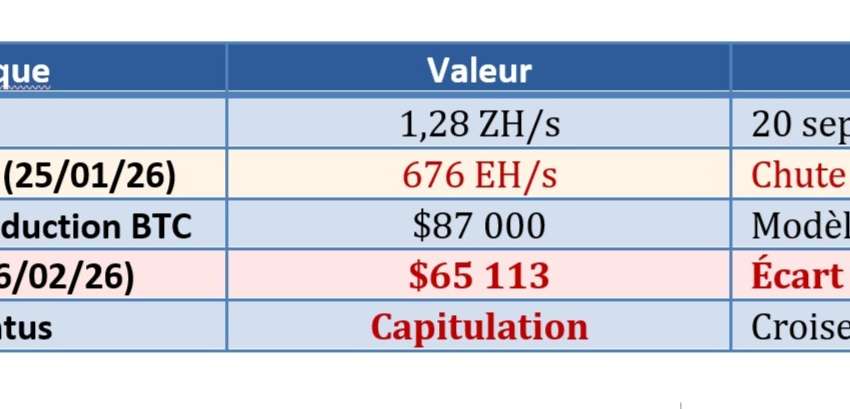

CTAs, large systematic trend-following funds, can trigger massive redemptions and forced selling during correlated drawdowns in tech indices like the Nasdaq-100. This poses a liquidity risk for crypto portfolios exposed to tech beta. The study models BTC’s exposure to the Nasdaq-100 using a time-varying beta derived from DCC-GARCH, empirically calibrated at 0.45. This indicates that a 10% Nasdaq drop statistically implies a 4.5% BTC drop, warranting a partial hedge.

Two hedging instruments are evaluated: Micro E-mini Nasdaq-100 futures (MNQ) and ProShares Short QQQ (PSQ). The MNQ, with its fine granularity, high liquidity, and low cost, is preferred over the PSQ inverse ETF due to the latter’s risk of “volatility drag” or temporal decay, making it unsuitable for hedges longer than a week. The optimal hedge ratio is calculated using the Minimum Variance Hedge Ratio, adapted for crypto. For a $689,000 BTC portfolio, this suggests shorting 19 MNQ contracts, resulting in a 105% hedge ratio. Institutions often use a slightly lower ratio (0.5-0.8) to retain residual positive delta.

Stress-testing through Monte Carlo simulations shows that a 19-contract MNQ short hedge can significantly reduce portfolio downside in various scenarios, improving VaR and Expected Shortfall by 42-45% while incurring minimal annual costs. Its implementation involves a pre-trade checklist, including conditional beta validation, instrument selection based on horizon, and position sizing with risk management protocols. A concrete example illustrates hedging a $345,000 BTC portfolio by shorting 10 MNQ contracts, representing a 110% notional hedge with an estimated margin of 1.4%.

The strategic synthesis combines a “Long Underlying + Short Proxy” approach. This “dual-track” strategy, supported by thermal satellite analytics for mining operations and macro analysis for hedging, aims for a higher Sharpe Ratio. The final recommendation is to accumulate BTC while tactically hedging the Nasdaq exposure using MNQ futures, anticipating a 39% improvement in the Sharpe Ratio over a 30-day horizon. This sophisticated strategy targets professional investors and family offices.