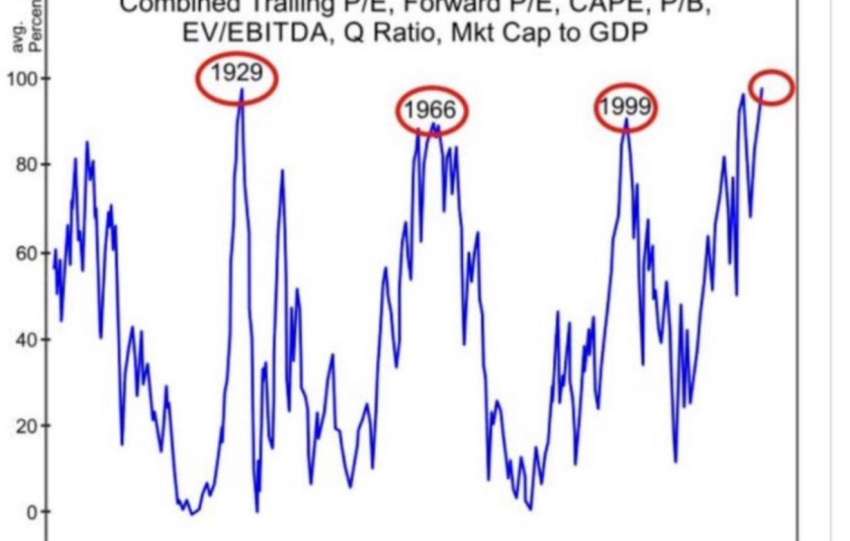

Analyse de marché

Analyse de marché

The current outperformance of gold (XAU) and mining stocks over the rest of the market (especially technology) is not a temporary anomaly. It results from the « double commoditization » of AI and software, which is destroying the monetization model of intellectual capital. As intelligence becomes a cheap and widely available commodity, the physical resources needed to sustain it—energy, metals, gold as the ultimate store of value—become scarce. We are seeing a shift away from long-duration assets (SaaS, AI startups) with increasingly uncertain future cash flows toward short-duration assets with intrinsic value.

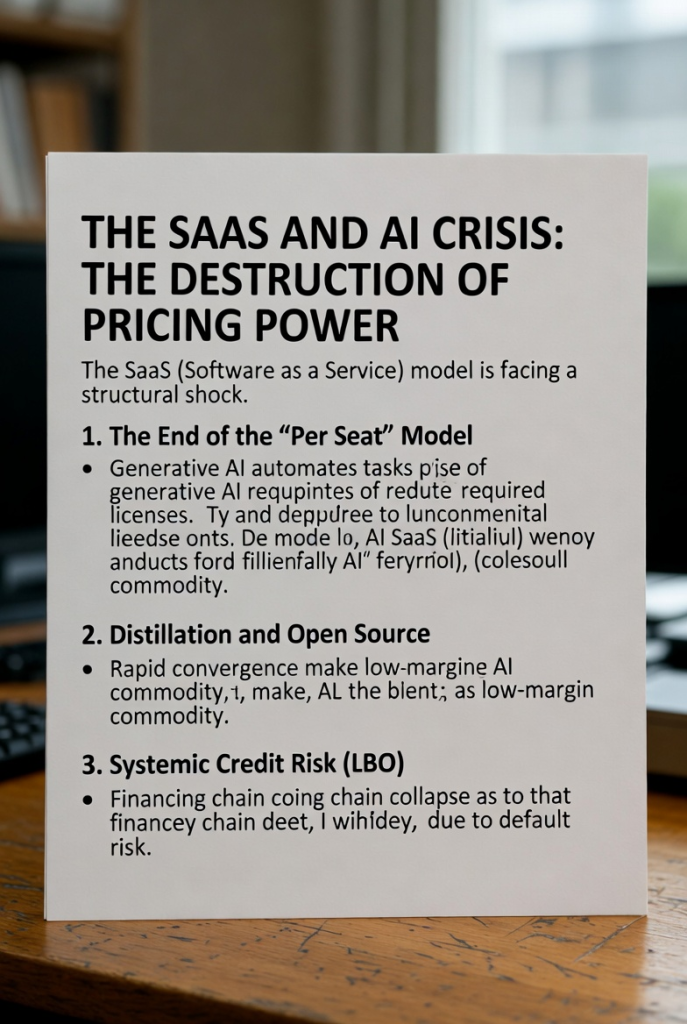

1. The SaaS and AI Crisis: The Destruction of Pricing Power

The SaaS (Software as a Service) model is facing a structural shock.

1.1. The End of the « Per Seat » Model

Generative AI automates cognitive tasks, reducing the number of required licenses. The model that underpinned valuation for the last 20 years is losing its core economic unit.

1.2. Distillation and Open Source

The rapid convergence of AI models causes technological advantage to evaporate faster than companies can monetize it. This turns AI into a low-margin commodity.

1.3. Systemic Credit Risk (LBO)

A large portion of the SaaS sector was financed through highly leveraged buyouts (LBOs). If the predictability of subscription cash flows collapses, the entire financing chain (private debt, banks) faces default risk.

2. Transition to Tangibility: Why Gold is the « Ultimate Collateral »

As « digital rents » depreciate, the market rediscovers the value of physical reserves.

• Gold as a hedge against AI uncertainty: Physical gold is unaffected by innovation scenarios or the success of API monetization. It is the only asset with zero counterparty risk in a world where « paper » registries (COMEX) are losing trust.

• Rule 401 and the collapse of the paper market: Events in the silver market (activation of Rule 401 on COMEX), enforcing cash settlement instead of physical delivery set a precedent for a « reality default. » Investors realized that paper contracts might not guarantee access to the metal, triggering a panic flight to physical gold and mining stocks.

• Infrastructure Hunger: The deployment of data centers requires massive amounts of copper, silver, and energy. Mining stocks today are the « shovel sellers » in the AI gold rush, but with real, tangible cash flows.

3. Three major factors are driving the price of gold upward

First, the kinetic conflict (USA/Iran), materialized through attacks on Aramco and threats to the Strait of Hormuz, is creating an oil supply shock and reintroducing an inflationary premium for which gold serves as a benchmark.

Second, the Shanghai premium has reached a critical level, with a substantial gap (more than 12–13%) between Western paper prices and physical prices on the Shanghai exchange, leading to large physical transfers of stocks from West to East.

Third, confidence in the dollar continues to erode due to an 80% expansion of M2 money supply since 2016 and its strategic weaponization (“Weaponization Risk”), prompting central banks (India, China) to aggressively accumulate physical reserves.

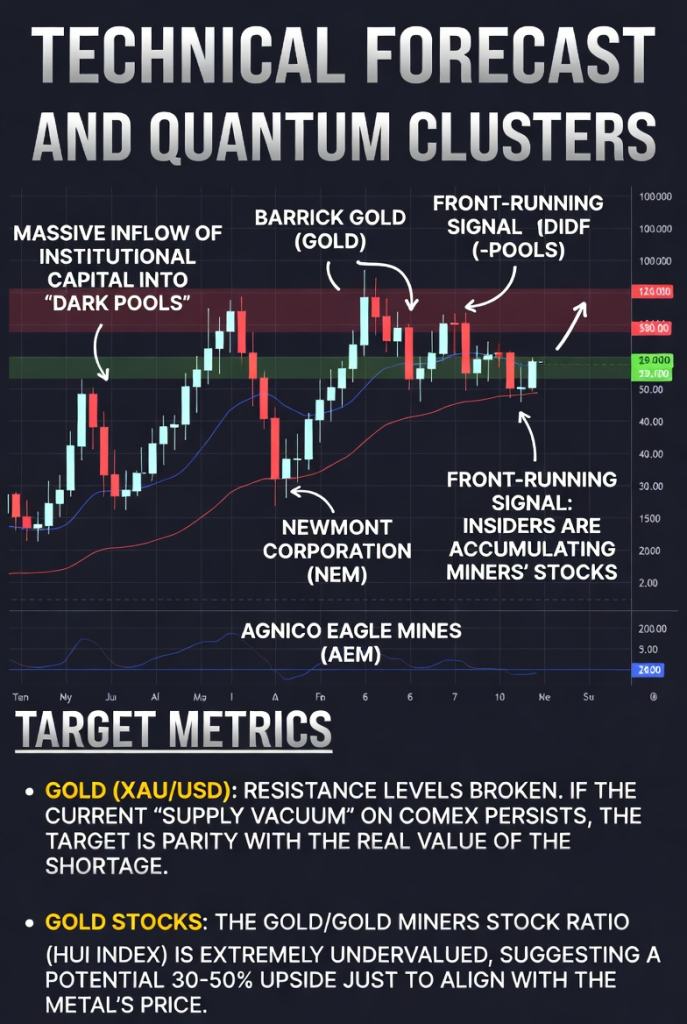

4. Technical Forecast and Quantum Clusters

Massive inflow of institutional capital into « Dark Pools » for gold mining stocks (Barrick, Newmont, Agnico Eagle).

• Front-Running Signal: Insiders are accumulating miners’ stocks, anticipating that the Federal Reserve will be forced to intervene to save the banking sector from the LBO/SaaS crisis. This will trigger a new wave of inflation, with gold as the only winner.

• Target Metrics:

– Gold (XAU/USD): Resistance levels broken. If the current « Supply Vacuum » on COMEX persists, the target is parity with the real value of the shortage.

– Gold Stocks: The gold/gold miners stock ratio (HUI Index) is extremely undervalued, suggesting a potential 30-50% upside just to align with the metal’s price.

Gold and gold stocks are showing the best results because they represent « ultimate liquidity » in a world where intellectual assets are commoditized and the financial structures built on them are overburdened with debt. The expected target for Bitcoin (digital gold) remains $89,722 as part of the overall flight to scarce assets.

RÉFÉRENCES ACADÉMIQUES ET SOURCES

Maynard Smith, J. (1982). Evolution and the Theory of Games. (Théorie des jeux évolutionnaire)

Mantegna, R.N. & Stanley, H.E. (1999). Introduction to Econophysics. (Mécanique statistique)

Kyle, A.S. (1985). « Continuous Auctions and Insider Trading. » Econometrica. (Market microstructure)

Steelldy Technologies (2026). Gotham Intelligence Platform – Geopolitical Risk Module.

Steelldy (2026). Steelldy Risk Engine 12.4 – Commodity Stress Testing Framework.

Bloomberg Intelligence (2026). Commodities Outlook – Gold & Silver Analysis.

Les Affaires/Morningstar (2026). Cours de l’or: à quoi s’attendre pour 2026 .

Zone bourse/Reuters (2026). Début record en 2026 : l’or s’envole .