Analyse de marché

Analyse de marchéMorgan Stanley warns that accelerating global AI adoption is fueling an unprecedented demand for electricity, potentially leading to a 20% U.S. power shortfall by 2028 if supply doesn’t match the exponential growth. Massive U.S. data centers, driven by major tech investments exceeding $400 billion by companies like Microsoft, Google, Amazon, and Meta for compute capacity by 2025, are projected to cause peak electricity deficits reaching 44 GW, equivalent to the power usage of over 3.3 million homes. Microsoft CEO Satya Nadella highlighted that the critical issue is now electricity, not compute, as AI chips risk being idle without sufficient power. Experts point to a fundamental mismatch between the fast pace of AI demand growth and the inherently slow timeline for developing new power infrastructure. This imbalance threatens to strain the U.S. grid, creating an “energy supply shock.” For example, Dominion Energy in Virginia, home to a major data center cluster, saw projected power demand surge from 40 GW to 247 GW in one year. Data centers currently consume 4% of U.S. electricity, a figure expected to rise to 12% by 2030. Morgan Stanley concludes that the non-linear, rapid growth of AI demand necessitates urgent rethinking of energy strategies by utilities, regulators, and tech firms across nuclear, renewable, and grid modernization sectors, emphasizing that power systems must adapt or the entire technological ecosystem will be impacted.

Morgan Stanley warns of a potential 20% US electricity shortfall for data centers by 2028, equating to a 44 GW deficit, largely spurred by AI infrastructure growth from tech giants. Data centers’ power consumption is projected to rise from 4% to 7-12% of total US electricity use. This power bottleneck forces acceleration towards non-traditional energy solutions like natural gas turbines and nuclear restarts to sustain AI hardware demands.

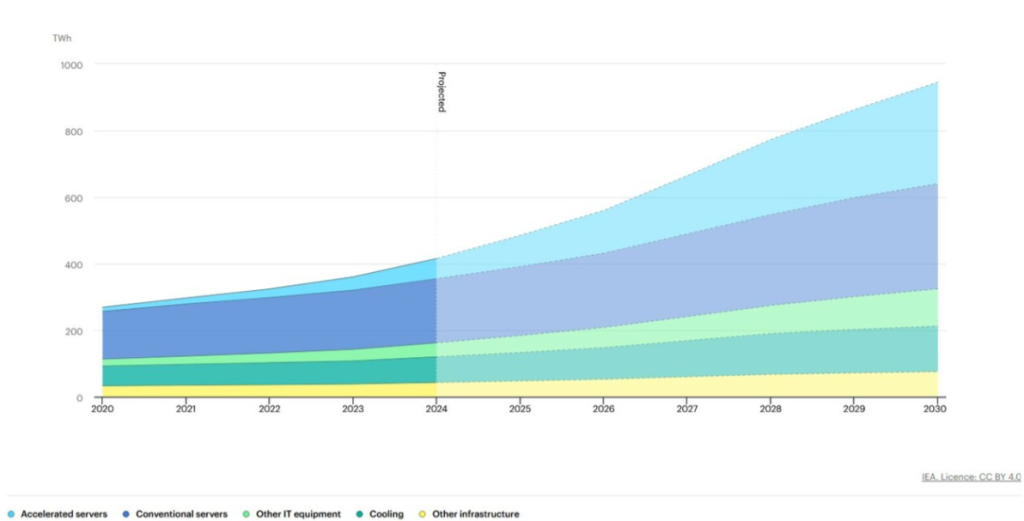

Global AI energy demands are surging due to massive data center electricity use, driven by AI workloads. In 2024, data centers consumed about 415 TWh (1.5% of global use). Projections estimate this will more than double to nearly 945 TWh by 2030 (under 3% globally), according to the IEA. Data center consumption has grown 12% annually since 2017, outpacing general demand. The IEA forecasts this growth rate will jump to 15% yearly through 2030, escalating over four times faster than the rest of the economy, with AI as the main catalyst.

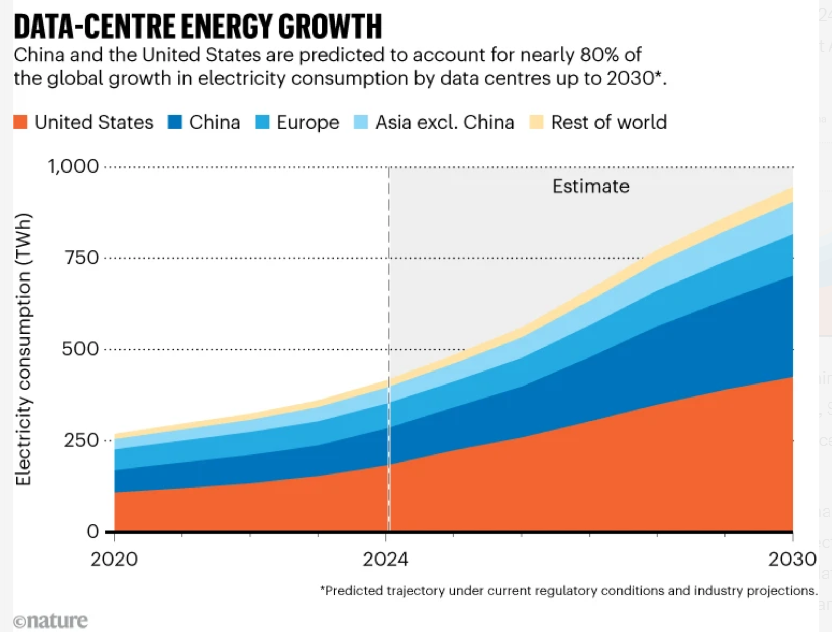

AI-specific servers are the main driver of global data center power consumption growth, projected to increase by 30% annually through 2030 and constitute nearly half of the total consumption rise. This contrasts with conventional servers growing at about 9% yearly, contributing only 20% to the net increase. Gartner forecasts that AI-optimized servers will rise from 21% of data center power use in 2025 to 44% by 2030. Other infrastructure components, including cooling, account for the rest, with cooling demands varying significantly based on facility efficiency. Geographically, the US and China lead both current use and future expansion. In 2024, the US consumed 45% (183 TWh) and China 25% of global data center power. Both nations are expected to drive roughly 80% of the global growth through 2030; the US is projected to increase consumption by 240 TWh (+130%) and China by 175 TWh (+170%). Europe’s growth is forecast to be more moderate at +45 TWh (+70%), while Southeast Asia is also emerging as a fast-growing hub.

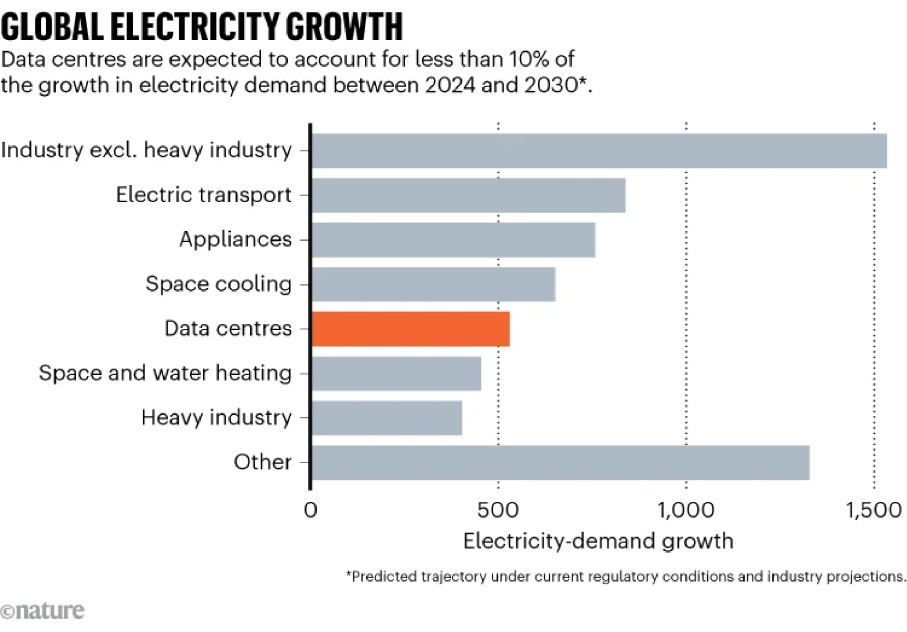

Global data center energy consumption is projected to surpass 500 TWh by 2026, nearing 2% of worldwide electricity use, largely driven by AI acceleration. While high-growth forecasts suggest faster increases, the IEA’s Base Case is the primary reference. Data centers are expected to account for less than 10% of total global electricity demand growth between 2024 and 2030, with industrial electrification, electric vehicles, air conditioning, and appliances being larger contributors. However, in specific concentrated markets, such as regions in the US, the rapid expansion of AI data centers is causing significant grid constraints, leading to increased direct power purchase agreements, reliance on natural gas backup systems, and efforts to restart nuclear power facilities.

Renewables, primarily solar and wind, are projected to meet around half of the new data center energy demand growth leading up to 2035, driven by corporate procurement. Natural gas and nuclear power, including future small modular reactors, will also be significant energy sources, especially in the US and China. While current data center emissions are about 180 Mt CO2, they are increasing but should remain a small fraction of global totals if clean energy adoption continues successfully. Modeling for 2035 shows wide uncertainty: a “Lift-Off” scenario with high AI growth could see demand exceeding 1,700 TWh, whereas significant efficiency gains (up to 15% reduction from the Base Case) or external bottlenecks could limit growth to around 700 TWh. Current efficiency improvements in hardware and software are being outpaced by soaring demand from both AI training and, increasingly, everyday inference usage. Overall, AI is rapidly reshaping global electricity consumption, with data centers becoming a major growth area, led by the US and China. While renewables are the primary supply solution, grid infrastructure presents the most immediate bottleneck. Continued rapid expansion through 2030 is anticipated, with long-term energy outcomes critically dependent on the trajectory of technological efficiency, supportive policy frameworks, and power sector investment. This analysis is based on IEA projections from April 2025.

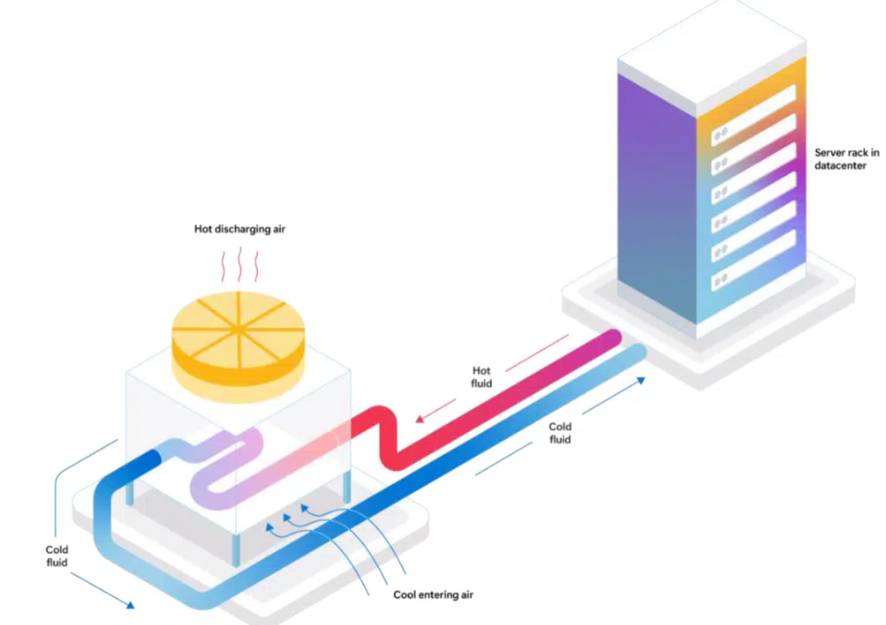

Extreme heat from high-density AI workloads, with GPUs exceeding 700W and racks reaching 50–140 kW, is forcing the rapid advancement of data center cooling beyond the limits of traditional air systems, which currently consume 7–30% of facility electricity. Liquid cooling solutions, specifically Direct-to-Chip (DTC) and immersion, are becoming essential, projected to drive the market from $870 million in 2024 to $10.7 billion by 2030 (CAGR ~52%). Adoption is skyrocketing, expected to cover 54% of servers by 2025 and 76% by 2026. DTC cooling is the most mature and scalable method, using cold plates to circulate liquid over processors, which lowers Power Usage Effectiveness (PUE) to approximately 1.07–1.13 and offers 15–20% power savings compared to air. Two-phase DTC, utilizing boiling fluids, enhances efficiency further. DTC is favored for retrofits and large deployments in 2025–2026 due to easier integration via Coolant Distribution Units (CDUs). Immersion cooling, submerging hardware in dielectric fluids, offers the highest thermal efficiency, potentially cutting electricity use by up to 99% in some configurations and supporting extreme densities with lower water usage (31–52% less than air) and extended hardware life. Two-phase immersion boiling provides rapid heat absorption. While upfront costs are higher, immersion is favored for new, high-density AI clusters. Cutting-edge innovations include microfluidic cooling—such as Microsoft’s planned 2025 etching of coolant-carrying microchannels directly into silicon dies—which lab tests show can remove heat three times more effectively than standard cold plates, preventing throttling in ultra-dense chips. Complementary technologies include advanced heat exchangers, spray cooling, and AI-driven predictive controls for dynamic optimization. Hybrid and emerging solutions, including Rear-Door Heat Exchangers (RDHx) and phase-change materials, are also contributing to the toolkit. Companies are commercializing high-capacity CDUs and microfluidic systems. These innovations are crucial for mitigating the projected massive surge in global AI energy demand (IEA forecasts ~945 TWh by 2030) by boosting efficiency and enabling higher compute utilization with less reliance on chillers. As of early 2026, DTC is dominant in new AI builds, while microfluidics and advanced two-phase systems are scaling in hyperscalers. Overall, liquid cooling is now fundamental to sustainable AI scaling, with future gains relying on integrating these technologies with advanced heat recovery systems.