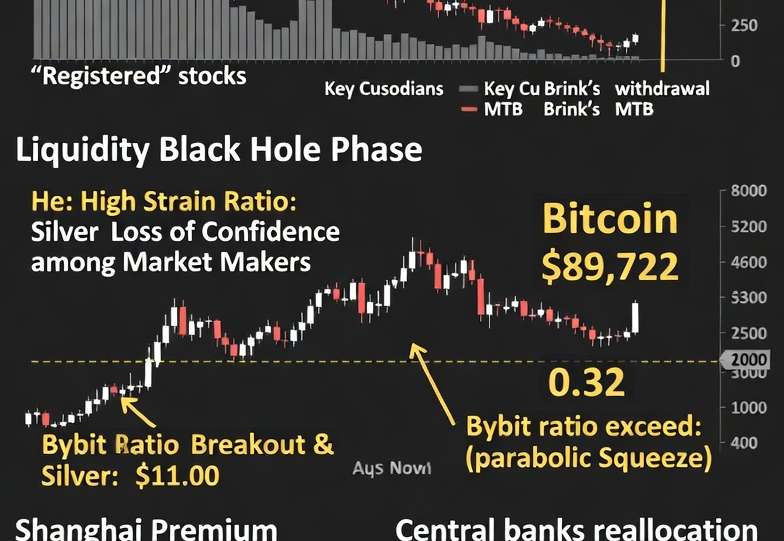

Analyse de marché

Analyse de marché

On June 30, 2026, @Nike (NKE) reported Q4 FY2026 results that appeared to show a spectacular rebound: Net Income of $1.1 billion, up 407% and far above the consensus of $0.13. However, this performance was not due to operational improvement but to an accounting artifact: a $986 million customs duty refund expected from a U.S. Supreme Court ruling on February 20, 2026, which invalidated tariffs imposed under the International Emergency Economic Powers Act (@IEEPA).

The reported EPS of $0.72 was 454% above the consensus of $0.13, but 72% of this ($0.52) came from the IEEPA refund. The adjusted operational EPS was only about $0.20. The refund also inflated gross margin by 900 basis points to 49.2%, and the effective tax rate fell artificially from 33.6% to 19.6%. However, total revenue declined 1% year-over-year, with a 12% drop in Greater China sales, a key concern. The Supreme Court‘s decision in “Learning Resources Inc. v. Trump” invalidated IEEPA tariffs, leading potential refunds of $175 billion or more for 2025. The Trump administration immediately imposed replacement tariffs under the Trade Act of 1974. Nike recorded the refund as a receivable, not cash.

The reported EPS of $0.72 is misleading: $0.20 operational and $0.52 from the refund. Excluding the refund, gross margin would have been stable. The effective tax rate drop to 19.6% is attributed to stock-based compensation and exceptional items, lower than the federal rate of 21%. Operational performance was weak: total revenue down 1%, Nike Direct down 7%, and Converse sales plummeting 32%. Greater China saw a 12% sales decline to $1.30 billion, with EBIT down 20%.

This underperformance is an anomaly, as competitors like Anta and Li-Ning are growing. China accounts for 11% of Nike’s revenue, posing currency and sales risks. Market reaction was negative, with the stock falling up to 8% in after-hours trading. Our analysis showed heavy institutional selling and high VPIN (0.62), indicating informed traders. The CFO’s communication, while accurate about results, downplayed the refund’s impact, an equilibrium in a bearish market. Ours simulations for FY2027 project a base case EPS of $2.40 (flat vs. adjusted FY2026).

The key risk is the non-recurring nature of the refund, making FY2026 EPS artificially high. EPS is artificially inflated by a non-recurring reimbursement. Operational performance declined: revenue -1%, China -12%, Digital -12%. Tax rate dropped abnormally from 33.6% to 19.6%. Risk lies in uncertainty over IEEPA reimbursement and China’s trajectory.