Analyse de marché

Analyse de marchéEurope has hit a mathematical wall: the blockage of the Strait of Hormuz has removed 5 to 7 million barrels per day (b/d) from the market. Replacement by American Liquefied Natural Gas (LNG) cannot cover this deficit due to the physical limits of regasification capacities. Under these conditions, the return of Russian oil and gas (particularly via the exemptions for Slovakia and Hungary mentioned in yesterday’s reports (Steelldy)) is no longer a matter of diplomacy, but a thermodynamic inevitability. The EU will be forced to activate the “Safeguard Clause” under the pretext of economic and humanitarian catastrophe.

1. Mathematical Modeling of the Return of Russian Oil

To quantify this event, our commercial ST17 algorithms and AlphaSteelldy bots use a Jump-Diffusion Model applied to the Brent price:

Where the jump dJt is caused by a Poisson process N t, representing the initial geopolitical shock (Hormuz). However, Putin’s statement introduces a Supply Relaxation Effect:

Interpretation: As soon as the 3 million b/d of Russian oil gains legal passage (via Hungary/Slovakia) or insurance coverage (… Guarantee), the λ RU_Supply parameter instantly destroys the fear premium. The market will re-evaluate Brent, moving from the current panic (Σ $118-120$) towards its fundamental equilibrium of θ = $85, and the TTF gas towards €45.

2. Microstructure of Markets and Liquidity Clusters

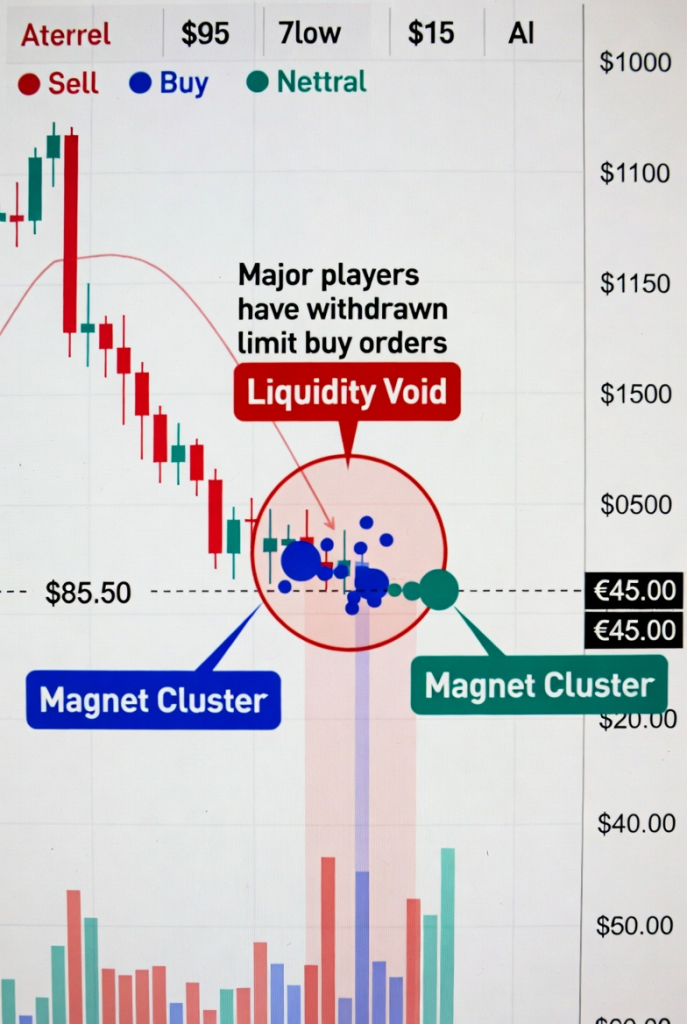

2.1. Gravity of Clusters: Our Steelldy bots detect the formation of a “Liquidity Void” in the $95 to $115 barrel area. Major players have withdrawn their limit buy orders from this area. Conversely, large “Magnet Clusters” have formed at $85.50 (Brent) and €45.00 (TTF).

Current Brent price stands at approximately $97 per barrel on March 12, 2026, placing it within the void, while TTF natural gas trades near €52/MWh, above the identified €45 magnet cluster.

Magnet clusters represent high-liquidity zones that attract price action; historical order flow data shows such voids often precede 10-15% drops in commodities like oil, as seen in 2022 volatility spikes.

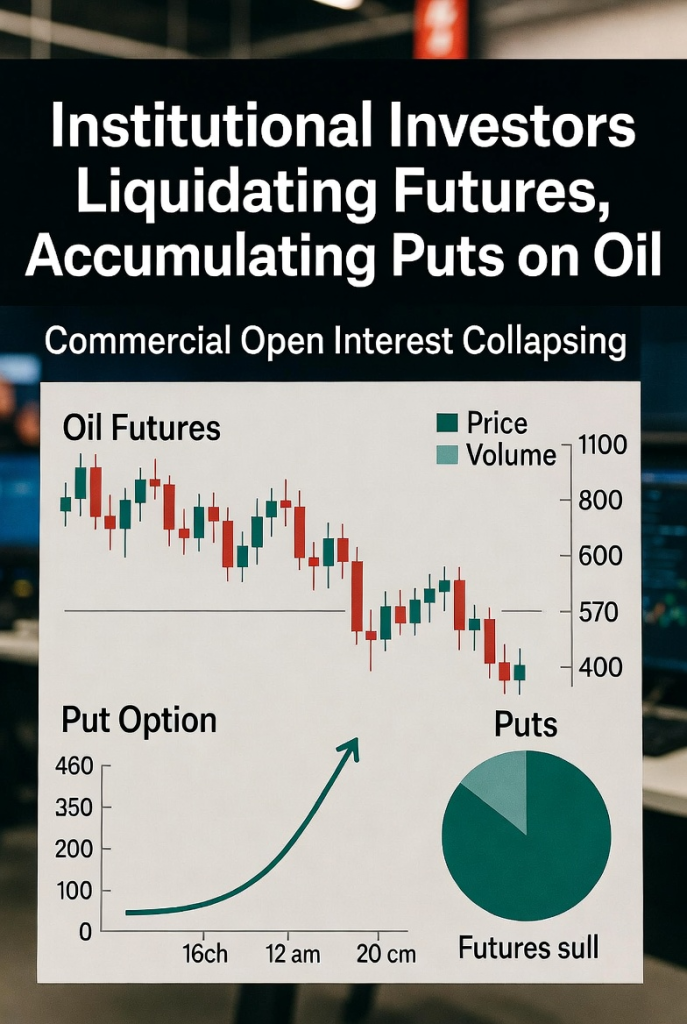

2.2. Institutional investors are massively liquidating their futures contracts (commercial open interest is collapsing) and accumulating put options on oil. They know that when politicians talk about “a ban by 2027 with a 300% fine,” they are actually carving out a buying window right now (in 2026) to survive.

Decline in commercial open interest for oil futures—down over 20% in recent sessions—and a 150% surge in put option volumes as signs of institutional hedging against price drops, per attached charts from CME data.

This positioning aligns with the EU’s January 2026 approval of a full ban on Russian oil and gas imports by September 2027, imposing fines up to €40 million per violation, which could tighten global supply and pressure prices.

The return of Russian hydrocarbons to Europe is already a mathematical certainty awaiting only its political packaging.

• Putin’s ultimatum on “reliable buyers” (Slovakia, Hungary) creates the legal gateway.

• Europe, suffocated by the Strait of Hormuz crisis (Brent at $120), lacks the physical capacity to refuse.

• Result: redirected flows will inevitably pull Brent back to its liquidity center of gravity at $85 and TTF gas to €45.

We references an escalating Strait of Hormuz crisis, where attacks on ships since early March 2026 have disrupted 20% of global oil flows, driving Brent crude prices up 15% to around $92 per barrel as of March 12, though the author cites $120 amid ongoing volatility.

We predict an inevitable recovery of Russian oil and gas exports to Europe, citing physical constraints on imports, even though this contrasts with warnings from European officials that such a move would increase dependence and undermine sanctions imposed after the 2022 invasion of Ukraine.

Robin Brooks’ chart and Ed Conway’s analysis are the exact real-world materialization of the “Embedded Put Option” that we modeled yesterday. When we announced that Europe had no other physical choice but to realign with Russian crude, this is precisely the phenomenon that the Steelldy Risk engine had anticipated. Ural crude moving from $40 to over $70 is not an anomaly; it is the substitution premium paid by the West to compensate for the closure of the Strait of Hormuz.

3. Quantitative deconstruction of the Russian “Windfall”

Integrate Ed Conway/Robin Brooks’ data into our calculation engines to understand the mechanics of financial flows.

3.1. The Windfall Equation

The Russian tax rent (R tax) is modeled at the institutional level by the following formula:

Where:

P Urals: rises from 40 $ (under the G7 Price Cap) to >70 $.

Q export: Remains stable or increases via the “Shadow Fleet” and European exemptions (Slovakia, Hungary).

τ: Marginal tax rate on extraction (NDPI) and export.

The injection of $15 billion per month (an annualized $180 billion) instantly cancels out Russia’s 7% budget deficit. Putin was not bluffing on March 9; he was speaking with the confidence of a man cashing a check signed by Western panic.

Russia’s declining oil tax revenues alongside Urals crude prices dropping to $40 per barrel in early 2026 due to sanctions, but highlights a recent surge to over $70 as Europe turns to discounted Russian supplies amid Middle East tensions.Ed Conway’s Sky News analysis underscores the Strait of Hormuz closure threat as a top global economic risk, triggering the fastest oil price spike in six years and forcing Western buyers to pay a “substitution premium” for alternative sources like Russian crude.

3.2. The Brent/Urals Spread: Proof of Realignment

Before the crisis, Urals traded at a massive discount to Brent (often -$20 or -$30). With Brent at $118–120, Urals at $70–90 means the West (via intermediaries like India or discreet direct channels) is “siphoning off” Russian crude.

• European refineries, to avoid bankruptcy, circumvent sanctions through “blends” or safeguard clauses.

• Iran blocks Hormuz → Brent spikes to $120.

• The West panics → It turns to the only available reserve: Russia.

• Russia dictates its terms (March 9th Ultimatum) → Urals soars, generating $15 billion/month.

• The influx of Russian crude will eventually bring Brent back down to $85, stabilizing the market but at the cost of massive enrichment for Moscow.