Analyse de marché

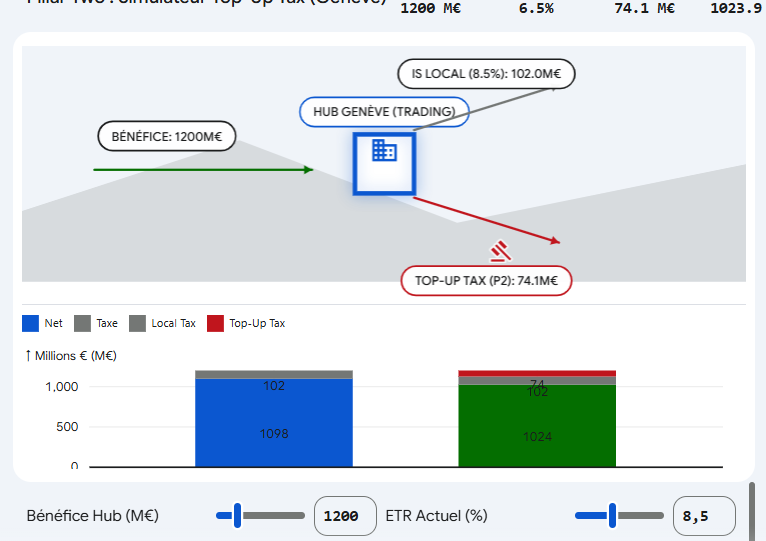

Analyse de marchéThe Real Asset Shifting (RAS) module (www.steelldy-indices.com) focuses on tangible assets, notably cross-border real estate. However, intangible assets (patents, trademarks, software, know-how, databases, client lists) are historically the main channel for profit shifting in multinational groups. Unlike tangible assets, intangibles do not significantly benefit from the Substance-based Income Exclusion (SBIE), are highly sensitive to transfer…

Carbon Credit Market

Carbon Credit Market