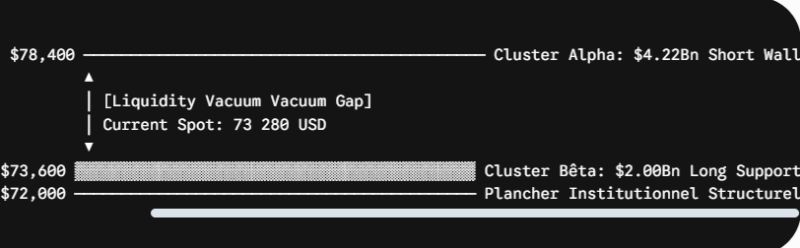

Analyse de marché

Analyse de marchéThe technical analysis posits a bullish outlook for gold, targeting $17,250/oz, underpinned by structural US fiscal dominance, accelerated de-dollarization, and a monetary re-evaluation of gold as an alternative reserve asset.

As of June 13, 2026, US gross public debt stands at approximately $39.2 trillion, with debt held by the public at around $31.6 trillion,…