Analyse de marché

Analyse de marché

The European Central Bank (@ecb ) exerts a dominant and stabilizing influence on eurozone sovereign spreads in 2026 through three main channels: the Transmission Protection Instrument (TPI) anti-fragmentation backstop (activated since 2022), the interest rate policy (25 bp hike on June 11, 2026: deposit rate at 2.25%, MRO at 2.40%), ongoing quantitative tightening (QT) and balance sheet reduction, and forward guidance.

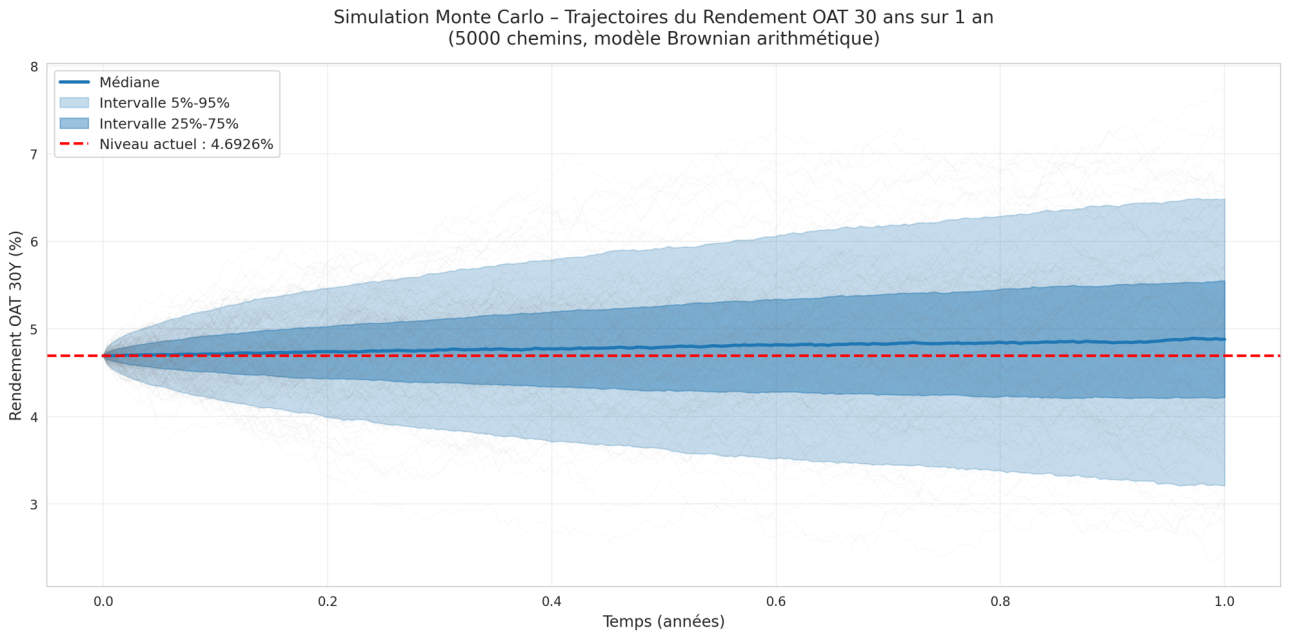

As of July 9, 2026, market data shows the 10-year OAT-Bund spread at ~77 bp (moderate, near post-2022 average of 60-80 bp), the BTP-Bund spread at ~78-80 bp (contained despite geopolitical tensions), and the 10-year OAT yield at ~3.75-3.81%. Despite France’s fiscal fragility (debt ~118% GDP, deficit ~5.1%), the spread remains contained thanks to the credibility of the TPI.

An activation could compress spreads by 30-60 bp in days, based on historical QE/PEPP/TPI effects. The theoretical decomposition models the sovereign spread as:

S = fundamental risk premium + fragmentation risk premium – β * ECB policy.

The TPI backstop channel is the most powerful in 2026, allowing unlimited sovereign bond purchases under specific conditions, historically compressing spreads by 40-80 bp.

The interest rate and forward guidance channel can widen spreads if fragmentation perception arises, but the “whatever it takes” signaling reduces risk premiums.

The QT channel increases net duration supply, potentially raising yields and spreads more on Bunds than OATs. Empirically in 2026, the ECB’s June 11 rate hike (inflation projected at 3.0%) kept the OAT-Bund spread around 70-77 bp despite French instability and Middle East conflict.

The TPI’s credibility acts as an implicit floor, preventing the spread from exceeding 85-90 bp, unlike the 150-200+ bp seen in 2011-2012 without a credible backstop. The QT effect has contributed an estimated +10-35 bp to Bund term premium, relatively helping contain the OAT-Bund spread.

Scenario analysis projects: a baseline (70-80 bp spread) with TPI status quo; moderate French deterioration (95-110 bp, 25-30% probability) with TPI on standby; severe shock (120-150 bp, 10-15% probability) with likely TPI activation compressing spreads by 40-70 bp; and normalization (50-60 bp, 20% probability) with no intervention.

The ECB effectively acts as a cap on spreads, but a French political deterioration or exogenous shock could push the OAT-Bund spread to 100-120 bp without ECB action.