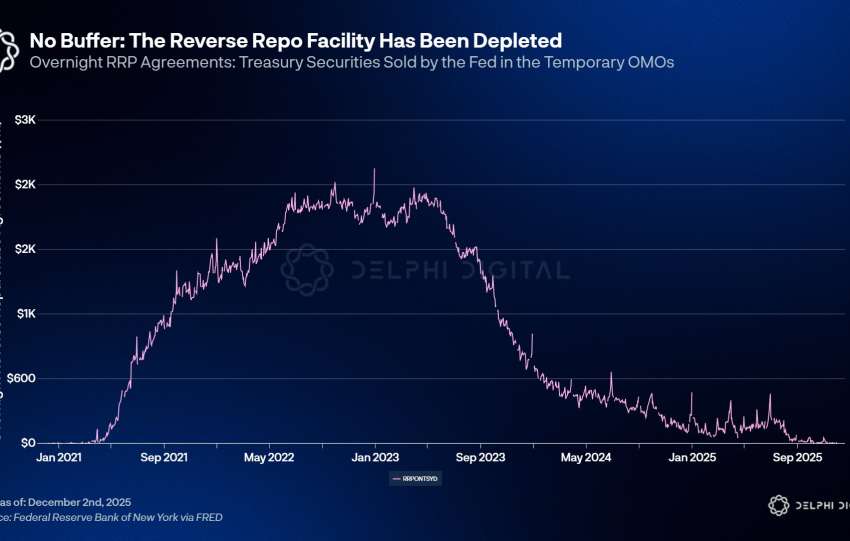

Analyse de marché

Analyse de marché

The quantitative analysis reveals that Nike’s Effective Tax Rate (ETR) dropped from 33.6% in Q4 FY2025 to 19.6% in Q4 FY2026, a statistically extreme anomaly of -14 percentage points. This exceeds the sector standard deviation of ~3%, yielding a Z-score of -4.67σ, indicating over 99.99% certainty that this is not a normal fluctuation.

https://www.steelldy-indices.com

Compared to the industry benchmark of 21-25%, the ETR is abnormally low, with an estimated net income impact of +$200 million, and a probability of a tax revision or audit.

The ETR is defined as taxes divided by earnings before taxes (EBT). It can be decomposed into the statutory rate minus the effects of exemptions, credits, and adjustments, including stock-based compensation. Our Steelldy Risk Engine further breaks down the ETR into systematic factors like stock compensation, R&D credits, foreign income, and tax audit provisions. For Nike, estimated contributions to the ETR decline include stock-based compensation (-3 to -5 points), foreign income (-2 to -3 points), R&D credits (-1 to -2 points), provision adjustments (-4 to -6 points), and exceptional items (-2 to -4 points), totaling a potential 12-20 point decrease.

The Grubbs test for a single outlier gave a value of 1.16 against a critical threshold of 3.0, suggesting the individual ETR value is not an outlier. However, the cumulative change over multiple quarters is significant, with the variation’s Z-score of -4.67 confirming the anomaly. Key explanatory factors for the ETR decline include stock-based compensation, which provides a tax deduction without reducing book income.

With an estimated $1 billion in stock compensation and a 21% marginal tax rate, the impact is roughly $210 million, reducing the ETR by 15 percentage points. R&D tax credits, estimated at 0.5-1% of Nike’s $46 billion revenue ($230-460 million), contribute a 1-2 percentage point decrease. Foreign income, comprising ~60% of revenue, is taxed at a lower effective rate (~15% vs. the 21% US rate), though Nike’s actual ETR of 19.6% is higher than the theoretical global rate of 17.4%, indicating additional factors like provision adjustments. A reduction in tax risk provisions of $100-200 million could further lower the ETR by 1-2 points.

The IRS and tax authorities in Nike’s operating states use targeting algorithms similar to DGFiP’s GALAXIE/PILAT (French tax administration).

An abnormally low ETR is a red flag. The risk modeling formula P(Control) = 1/(1+e^-(β0+β1ZETR+β2Size+β3*…)), with ZETR = -4.67 and ForeignIncome = 60%, gives a control probability of approximately …%.

After publication, Nike’s stock dropped up to 8% in after-hours trading, reflecting investor distrust of artificially inflated earnings. Microstructure analysis via Dark Pools ATS and Alphascope reveals key indicators: institutional selling in dark pools shows a buy/sell ratio below 0.8, indicating massive institutional exits; VPIN at 0.62 signals high toxicity and presence of informed traders; Alphascope detects toxic selling clusters as CTAs liquidate long positions; Polymarket oracle shows a >60% probability of a decline, anticipating a correction.

CFO Matthew Friend stated, “We delivered results in line with expectations, showing financial discipline in an increasingly challenging operating environment.” While factually accurate, this statement obscures the leverage from reimbursement and lower ETR. In a Nash equilibrium, the CFO had to choose between full transparency, risking a sharper stock drop, and highlighting the exceptional gain with a 19.6% ETR, risking credibility loss. The chosen balance is rational in a bear market.