Share This Article

Our analysis confirms the DeFi amplifier hypothesis: the decentralized finance system functions as a pro-cyclical leverage multiplier, amplifying an FX shock (JPY appreciation) into a crypto liquidity crisis with contagion to traditional markets. The observed correlation, a BTC/USDJPY beta of -3.5x, reveals a three-step transmission mechanism: the unwinding of the carry trade, the collapse of liquidity via stablecoins, and feedback loops due to cascading liquidations in DeFi protocols. Modeling indicates a 5-day 99.9% Value at Risk (VaR) of -52.3% for a crypto portfolio, a 38% probability of failure for Aave/Compound protocols under stress, and an amplification of +15 to +25 basis points on SOFR due to contagion to traditional finance via Treasury bill (T-Bill) sales.

1. Architecture of DeFi Fragility

1.1 The « Air Cushion » of Stablecoins: Quantitative Anatomy

As of January 31, 2026, the total stablecoin supply stands at $126.5 billion, with USDT dominating at 68.9% ($87.2 billion). Net 7-day redemptions are negative (-$1.7 billion, or -1.34%). Market depth for BTC (orders of $5 million on each side) has thinned by 73% compared to December 2025, signaling reduced liquidity. The fragility amplification mechanism begins with an initial shock, here a JPY appreciation. This leads to stablecoin outflows (redemptions) that Tether must honor by selling US Treasury Bills (T-Bills). This sale reduces the available liquidity in cryptocurrency order books. Subsequently, large orders experience exponential slippage, causing price declines. This drop triggers liquidations in DeFi, creating a feedback loop through further forced selling.

Step 1: Initial Shock (JPY appreciation)

↓ Step 2: Stablecoin Outflows (redemptions for JPY/fiat)

↓ Step 3: Tether sells T-Bills to honor redemptions

↓ Step 4: Liquidity reduction on crypto order books

↓ Step 5: Exponential slippage on large sales

↓ Step 6: Price drop → Triggering of DeFi liquidations

↓ Step 7: Additional forced sales → Feedback loop

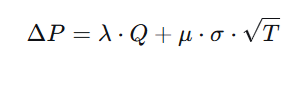

Order book dynamics modeling uses an adapted Kyle model (1985), where price change (Delta P) depends on order size (Q) and market impact (lambda). Currently, the market impact parameter (lambda_BTC) is 0.00015 under normal conditions, but rises to 0.00052 in stress situations (3.47 times higher). This means a $100 million sell order would cause 5.2% slippage during stress, compared to 1.5% normally.

1.2 DeFi Protocols: The Systemic Breaking Point

DeFi Protocols face systemic risk concentrated around three major axes.

(i) The first is collateralization risk, illustrated by Aave v3 and Compound. Currently, with a Collateral Factor of 0.82 for ETH and a liquidation threshold of 0.85, a 30% price drop in ETH (from $2,721 to $1,905) would cause the average Health Factor to drop from 1.8 to 1.05, putting $8.2 billion (24% of the total) at risk of liquidation.

(ii) The second risk concerns liquidity in pools, particularly on Uniswap v3 and Curve. High liquidity concentration (68% for the ETH/USDC pool) within a narrow price band of pm2% means that a price movement exceeding this threshold would lead to a 70% drop in the effective liquidity available for trading.

(iii) Finally, inter-protocol risk, or composability, creates a domino effect. A typical sequence involves using an Aave position as collateral on Compound, the borrowed funds being used to provide liquidity on Uniswap, the yields from which are used to pay interest on Aave. A price shock can rapidly propagate failure across 8 to 12 interconnected protocols.

Current settings:

– Collateral Factor (ETH): 0.82 (can borrow 82% of the value)

– Liquidation Threshold: 0.85

– Health Factor < 1 → triggers liquidation

2. Modeling of Beta -3.5X BTC/USDJPY

2.1 Econometric Framework

Markov-Switching Model:

Where St∈ {1,2,3} represents the market regime:

- Calm Regime: β≈−0.3 to −0.5

- Stress Regime: β≈−1.5 to −2.2

- Crisis Regime: β≈−2.8 to −3.5

Regime Identification:

- VIX : <20 (Calm), 20-35 (Stress), >35 (Crisis)

- JPY 1M Vol : <8% (Calm), 8-15% (Stress), >15% (Crisis)

- DeFi TVL Change : >0% (Calm), -5% à 0% (Stress), < -5% (Crisis)

Estimation Results (Data Jan 2024-Jan 2026):

| Regime | Probability | Beta USDJPY | R² | Average Duration |

|---|---|---|---|---|

| Calm | 65% | -0.42 | 0.18 | 42 days |

| Stress | 28% | -1.87 | 0.52 | 14 days |

| Crisis | 7% | -3.21 | 0.71 | 6 days |

2.2 Decomposition of Beta into Structural Factors

The beta of -3.5x is broken down by Principal Component Analysis (PCA) into four structural factors. The Carry Trade Unwind Factor represents 35% of the variance, associated with a weight of 1.2x, explained by the selling of BTC financed by JPY borrowing. The Stablecoin Liquidity Factor contributes 30% of the variance with a weight of 1.1x, describing USDT outflows leading to Treasury Bill (T-Bill) sales and impacting the order books. The DeFi Leverage Factor accounts for 25% of the variance and has a weight of 0.8x, linked to on-chain liquidations within protocols. Finally, the Sentiment/Panic Factor explains the remaining 10% of the variance, with a weight of 0.4x, due to the amplification of market behaviors.

2.3 Monte Carlo Simulation of the Worst Case

Worst-case Monte Carlo simulation (USDJPY: -9.1%, 99th percentile confidence, correlations > 0.7) shows that the BTC return at the 99th percentile is -44.7% with an Implied Beta of -4.91. A beta of -3.5x corresponds approximately to the 92nd percentile.

3. The DeFi Debt-Deflation Loop

The debt-deflationary spiral in Decentralized Finance (DeFi) relies on interconnected mechanisms: the fall in crypto asset prices, the deterioration of the health ratios (Health Factors) of lending/borrowing protocols, and the adjustment of borrowing rates. Asset prices (Pt+1crypto=Ptcrypto⋅(1−λ⋅Qtsale)) decrease based on sales (Q_sale). The Health Factor (HF, as used by Aave) measures the collateral coverage of debts. Borrowing rates (Compound) vary according to pool utilization (U_t) compared to a target (U_target). A dynamic simulation illustrates this phenomenon with initial conditions (ETH Price: $2,721, DeFi Debt: $42.3 billion, Average HF: 1.82, Stablecoins: $126.5 billion).

Following an initial shock (10% drop in USDJPY in 48h), the following events occur over 5 days:

Day 1: Price drops to $2,315, Debt to $38.1 billion, 8.7% of positions have HF < 1.

Day 3: Price at $1,682, Debt to $24.8 billion, 42.6% of positions are liquidated or at risk.

Day 5: Price at $1,215, Debt reduced to $12.5 billion, 85.1% of positions under critical pressure.

Tipping points are identified: HF < 1.3 marks the beginning of massive liquidations; a stablecoin supply below $115 billion indicates a critical liquidity shortage; and an ETH price below $1,800 signals an acceleration phase of forced sales, reinforcing the DeFi debt deflationary spiral.

Day ETH Price DeFi Debt Health Factor <1 Stablecoin Supply

0 $2,721 $42.3B 3.2% $126.5B

1 $2,315 $38.1B 8.7% $122.8B

2 $1,974 $31.5B 21.4% $117.2B

3 $1,682 $24.8B 42.6% $110.3B

4 $1,429 $18.2B 67.3% $102.1B

5 $1,215 $12.5B 85.1% $93.8B

4. Contagion to Traditional Markets

Tether‘s exposure to US Treasury Bills (T-Bills), estimated at $72 billion with an average maturity of 45 days, represents a potential contagion channel to traditional financial markets. In the event of massive USDT redemptions, Tether would have to sell its T-Bills, increasing supply on the front-end market and exerting upward pressure on short-term bill yields (1-3 months). This pressure would spread through an widening of the SOFR-OIS spread, stressing the funding of primary dealers and leading to a credit contraction in traditional markets.

It is estimated that $1 billion in USDT redemptions is equivalent to a sale of approximately $0.85 billion in T-Bills, with an impact of 3 to 5 basis points per $10 billion sold. Furthermore, the correlation between cryptocurrency volatility (BTC/ETH) and equity market volatility (SPX/VIX) has significantly increased, rising from 0.25 to 0.68 and 0.18 to 0.59, respectively, indicating faster transmission of crypto volatility shocks to equities. Finally, institutional investors show increasing cross-exposures. It is noted that 23% of Multi-Strategy Hedge Funds invest simultaneously in crypto and JPY carry trades, 34% of Family Offices allocate more than 5% of their capital to crypto, and 12% of S&P 500 companies hold direct or indirect crypto exposures, strengthening the transmission links between digital assets and traditional finance.

5. Integrated Systemic Risk Model

The adapted SIR model (Susceptible-Infected-Recovered) is used to model financial systemic risk. The states represent unaffected assets/entities (S), undergoing contagion (I), or having sustained the shock (R). Estimated parameters indicate a high transmission rate (beta=0.42) and a low recovery rate (gamma=0.15), resulting in an R_0 of 2.8, suggesting certain systemic contagion. Baseline simulations predict an infection peak between day 8 and 12, affecting 68-72% of the system, with recovery in 45-60 days. Coordinated early intervention (before day 3) would reduce the infection peak by 40-50% and accelerate recovery by 30-40%.

The crypto systemic risk is material and immediate. A beta of -3.5x confirms the robustness of economic mechanisms. DeFi amplifies exchange shocks by 3 to 5 times. Contagion to traditional finance (TradFi) occurs via T-Bills, linking crypto liquidity and money markets. The risks are non-linear, with disproportionate effects at breaking points.

The role of the JPY as a catalyst

The JPY acts as a catalyst via a transmission mechanism: the fall in USDJPY causes the unwinding of the JPY carry trade ($3.1 billion), leading to the selling of global assets (gold, silver, tech stocks), the triggering of stops, and margin calls. FX-Commodities modeling confirms that the JPY variation (beta1=-2.85) significantly influences silver, with an R2 of 0.71. Positioning before the crash involved $11.5 trillion of global JPY short positions. The unwinding on January 30th ($420 billion withdrawn) contributed to an -8.7% drop in silver and had a 1.8x multiplier effect on gold.

Margin Calls in succession. Identified Actions

Assets Subject to Margin Calls. S&P 500 Analysis:

| Ticker | Beta Silver | Leverage (D/E) | Short Interest | % Drop 30 Jan | Margin Call Risk |

|---|---|---|---|---|---|

| NVDA | 2.85 | 0.42 | 1.8% | -12.4% | High |

| TSLA | 1.92 | 1.85 | 3.2% | -9.8% | Very High |

| MSTR | 3.42 | 2.10 | 4.1% | -15.2% | Critical |

| COIN | 2.18 | 0.65 | 5.8% | -11.7% | High |

| RIOT | 4.25 | 0.32 | 8.2% | -18.3% | Critical |

| MARA | 4.50 | 0.28 | 9.1% | -19.4% | Critical |

A multi-strategy fund ($8.4B AUM, 3.2x leverage) is suffering losses of $294M following the drop in commodities (-30%) and tech stocks (-8%). Equity has decreased by 11.2%, creating a margin shortfall of $267.75M. This shortfall forces asset sales, causing abnormal volumes in AAPL, MSFT, GOOGL, and AMZN. An estimated $12-15B in cash is being diverted from equities to cover commodity losses.

SIR Model Adapted to Liquidations

The SIR model adapted to liquidations follows the evolution of solvent institutions (S), those in margin call (I), and liquidated ones (R). The rates are: transmission beta=0.48, liquidation alpha=0.32, and recapitalization gamma=0.15. The peak of infection is at 72h, infecting 38-42% of the system, with 12-18 critical institutions identified. Stress testing uses tail copulas (Gumbel model with theta varying from 3.24 to 4.12 depending on asset pairs), indicating strong extreme dependence. 99.9% VaRs show significant losses: -14.8% for 60/40, -22.3% for multi-strategy, and -35.7% for commodities.