Analyse de marché

Analyse de marché

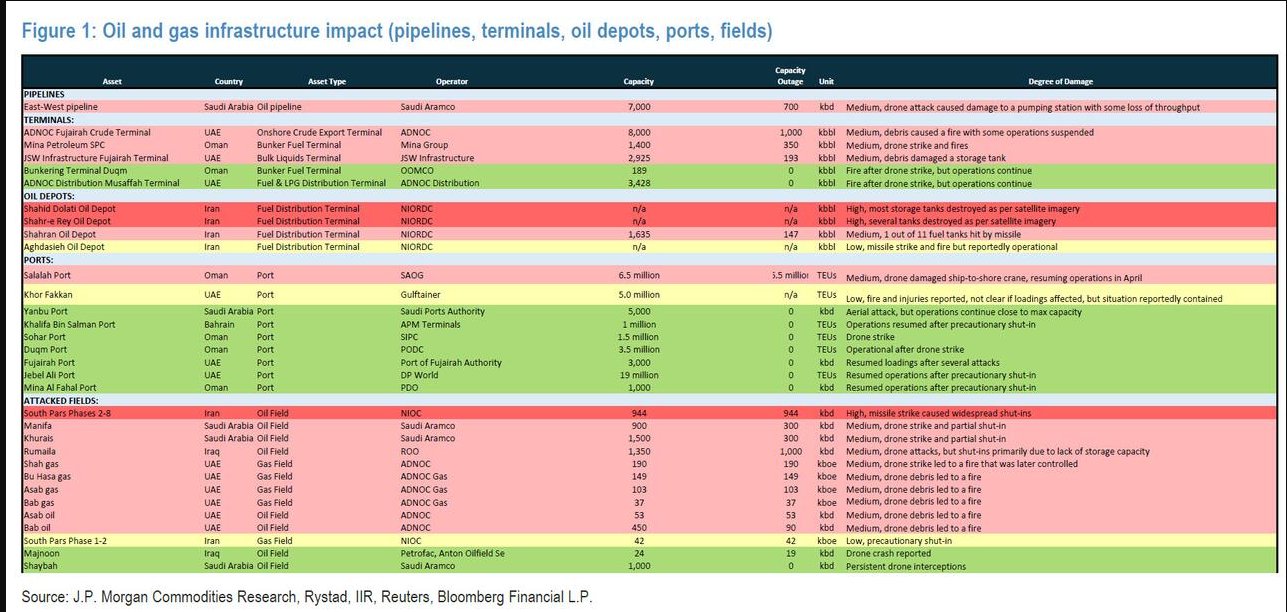

A JP Morgan Commodities Research table listing specific oil and gas assets hit across the Middle East, including pipelines, terminals, ports, depots, and fields in Saudi Arabia, UAE, Iran, Iraq, and Oman.

The table details drone strikes, missile attacks, and fires causing capacity outages, with examples like partial shutdowns at Saudi East-West pipeline, full disruptions at Iranian South Pars oil fields, and varying impacts on UAE/Saudi ports.

Posted amid regional conflict, it highlights energy supply risks with data on operators, capacities, and damage degrees, drawing replies noting potential reconstruction opportunities.

(a) The 2026 oil crisis exceeds Covid‘s scale as a persistent supply shock, with 12-15M b/d of liquids removed via Strait of Hormuz disruptions and Qatar LNG damage offline 3-5 years, forcing price-driven demand destruction rather than policy reversals.

(b) A fragile April 8 ceasefire has failed to fully reopen Hormuz due to Iranian restrictions, mines, and tolls, amid ongoing Lebanon tensions, amplifying shortages in oil, gas, fertilizers, and plastics that hit Asia hardest first before spreading globally.

(c) Markets underpricing duration — energy futures assume quick fixes while real indicators like diesel spikes and corporate margin warnings signal broader recession risks through H2 2026 via systemic supply chain repricing.