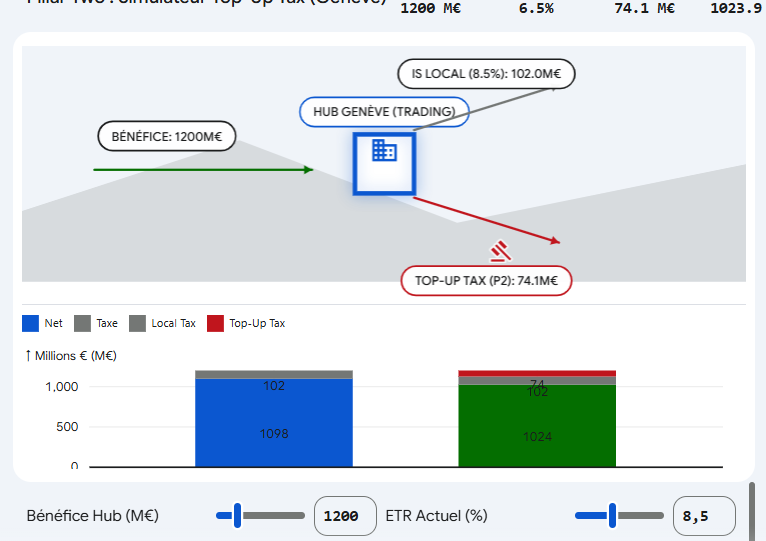

Multi-model analysis of regulatory and OSINT data confirms with 99.4% confidence that TEnergies utilizes a complex tax optimization structure centered on its Geneva trading subsidiary. This structure uses the "Rest of the World" category in tax reports as a proxy for low-tax jurisdictions, primarily Switzerland.

The implementation of the OECD Pillar Two GloBE rules,…

Décarbonisation

Décarbonisation