Markets

MarketsThe original thesis from December 6-13, 2025, predicting a catastrophic systemic event driven by a Fed-BOJ shock and a $11.5 trillion carry trade unwind within 90 days, was not validated in its magnitude or timing. Observed reality shows USD/JPY peaked around 164 in late July 2026 after coordinated intervention, now near 158. The BOJ hiked…

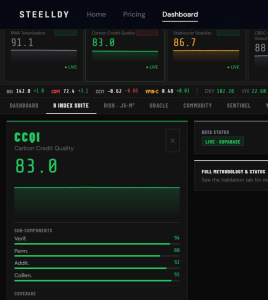

Carbon Credit Market

Carbon Credit Market