Analyse de marché

Analyse de marché

IATA Director General Willie Walsh warning that jet fuel supply restoration in the Middle East will require months even after Strait of Hormuz reopening, due to major refining capacity damage.

The statement follows a US-Iran two-week ceasefire announced by President Trump, conditional on safely reopening the Hormuz Strait, which triggered a drop in oil prices below $100 per barrel.

Asian airlines have responded to the supply squeeze and doubled jet fuel prices by cutting flights, carrying extra fuel loads, and adding refueling stops amid the regional conflict.

This follows a February 2026 Middle East conflict that disrupted ~20% of global oil flows through Hormuz and targeted refineries, with a recent US-Iran ceasefire enabling potential reopening but not quick restoration of refined products.

Airlines face prolonged high jet fuel costs, as seen in projections like Delta’s $2 billion Q2 impact, likely sustaining elevated fares and supply pressures for global aviation.

The refinery damage from the 2026 Middle East conflict (triggered by U.S.-Israeli strikes on Iran starting February 28)

Extensive damage to Middle East oil refineries, stemming from the 2026 conflict initiated by U.S.-Israeli strikes on Iran on February 28, is causing a prolonged global jet fuel shortage, according to IATA Director General Willie Walsh. Drone and missile strikes impacted energy infrastructure across at least nine countries, specifically hitting refineries hard.

Approximately 2.4 million barrels per day (bpd) of refining capacity, representing 10-12% of global capacity at its peak, was taken offline across about 20 Gulf coast plants. The core issue is the mismatch between crude oil recovery and refinery repair timelines. Crude production can normalize faster, but repairing complex refining units, particularly those producing jet fuel and distillates, takes months. Middle Eastern refineries are critical global suppliers of refined products, creating a severe bottleneck.

Key damaged facilities include:

Bahrain’s Sitra Refinery (448,000 bpd). Severely damaged by Iranian missiles, with 50% capacity affected, requiring several months for ramp-up.

Saudi Arabia’s Ras Tanura Refinery (550,000 bpd). Halted by a drone attack but restarted within weeks.

Kuwait’s Refineries (Mina Al-Ahmadi and Mina Abdullah). Over half the country’s capacity affected by drone strikes and fires, leading to significant output reduction.

Iran’s Tehran Refinery (250,000 bpd). Suffered high damage to fuel tanks, with potential one-month recovery. Additional damage to petrochemical and LNG facilities (like potential years-long disruption at Qatar’s Ras Laffan) has compounded refined product scarcity.

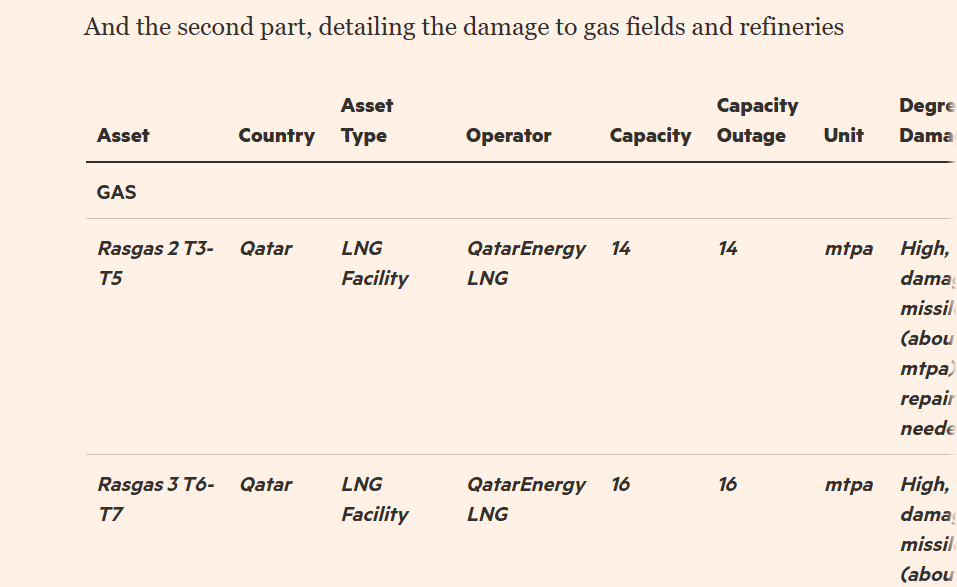

The asset damage table details significant disruptions to the energy infrastructure, particularly in Qatar, the UAE, and Bahrain.

Gas Assets: Major damage concentrated on Qatari LNG facilities operated by QatarEnergy LNG. The Rasgas 2 (T3-T5) and Rasgas 3 (T6-T7) facilities sustained “High” damage from missile strikes, specifically affecting trains 4 and 6, necessitating long repairs and causing outages of 14 mtpa and 16 mtpa, respectively. In the UAE, the Habshan Complex experienced “High” damage resulting in one fatality. Several Qatargas and Rasgas trains sustained “Medium” damage due to drone strikes following precautionary shut-ins, leading to slow restarts. UAE facilities in Abu Dhabi (ADGAS LNG) faced “Low” impact, mainly from falling debris after precautionary shutdowns.

Refineries: Bahrain’s Sitra Refinery suffered “High” damage, with 50% capacity severely affected, requiring several months for recovery. Iran’s Tehran Refinery sustained “High” damage to fuel tanks but expected operational return within a month. Kuwati refineries (Mina Al Ahmadi and Mina Abdulla) faced “Medium” damage from drone attacks, causing partial or full outages. Iraq’s Lanaz Refinery also saw production halt due to drones and fire, with an expected one-month restart time. Many other refineries across the UAE, Qatar, Kuwait, Saudi Arabia, Oman, and Iraq reported “Low” impact, precautionary shut-ins following incidents (drones or missiles), or continued near-full operation despite reported attacks (e.g., Saudi Aramco’s SATORP, Riyadh, and Ras Tanura, and Oman’s Duqm). Israeli Haifa Refinery showed no serious satellite-observed damage post-missile strike, and several other facilities restarted successfully or sustained minimal operational loss.

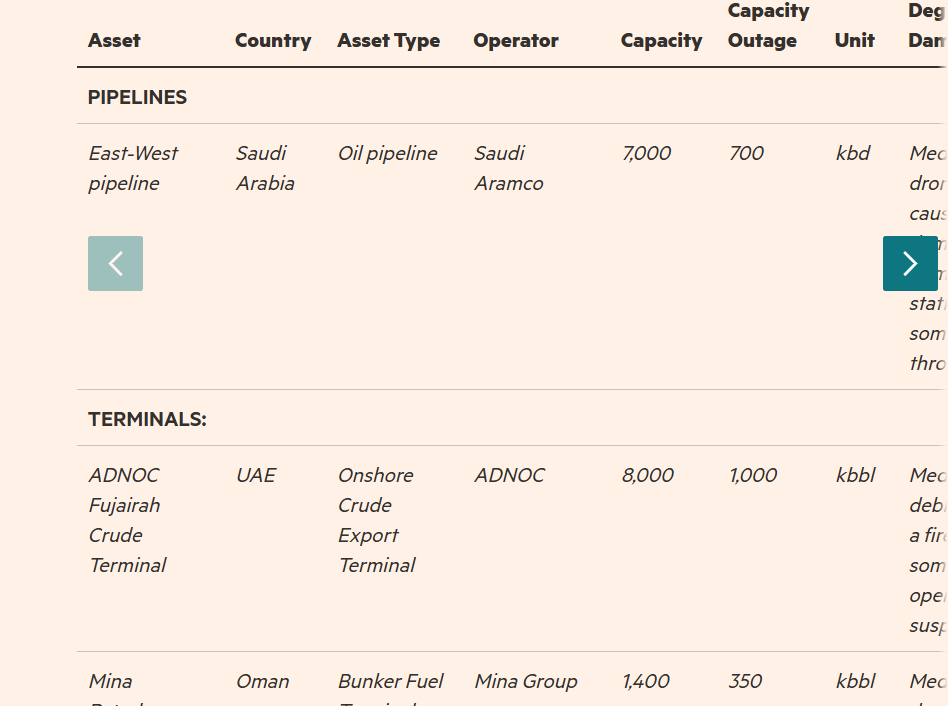

The core of the text details the impact of attacks on oil and gas infrastructure across the Middle East. Damage levels are categorized, with serious damage italicized and severe damage italicized and bolded.

Pipelines.The East-West pipeline in Saudi Arabia, operated by Saudi Aramco, experienced medium damage from a drone attack on a pumping station, resulting in a 700 kbd throughput loss out of a 7,000 kbd capacity.

Terminals. Several terminals faced disruptions: ADNOC Fujairah Crude Terminal (UAE) sustained medium damage and a 1,000 kbbl outage due to a debris-caused fire. Mina Petroleum SPC (Oman) reported medium damage from a drone strike and subsequent fire. JSW Infrastructure Fujairah Terminal (UAE) sustained medium damage to a storage tank from debris. Two terminals, Bunkering Terminal Duqm (Oman) and ADNOC Distribution Musaffah Terminal (UAE), experienced fires following drone strikes but maintained operations.

Oil Depots. The most severe impacts were seen at Iranian depots: Shahid Dolati and Shahr-e Rey Oil Depots (Iran) suffered high damage, with satellite imagery indicating most or several storage tanks destroyed, respectively. Shahran Oil Depot (Iran) had medium damage after a missile strike hit one of 11 fuel tanks, causing a 147 kbbl outage. Aghdasieh Oil Depot (Iran) reported low damage from a missile strike, but remained operational.

Ports. Port operations faced various levels of disruption: Salalah Port (Oman) sustained medium damage when a drone struck a ship-to-shore crane, with operations expected to resume in April. Khor Fakkan (UAE) reported low-level disruption from a fire. Ports in Yanbu (Saudi Arabia), Khalifa Bin Salman (Bahrain), Sohar (Oman), Duqm (Oman), Fujairah (UAE), Jebel Ali (UAE), and Mina Al Fahal (Oman) all reported incidents including aerial attacks or drone strikes, but most either continued operations close to capacity or quickly resumed service after precautionary shutdowns.

French intelligence reportedly estimated ~30% of Middle East refinery infrastructure was damaged or destroyed early on. While a ceasefire is in place and some high-throughput facilities like Ras Tanura have restarted, analysts, including JPMorgan’s Natasha Kaneva, state that extensive repairs mean jet fuel supply and prices will not normalize quickly, aligning with Walsh’s assessment that the lag in refining recovery is the central challenge for aviation fuel supplies. Exact repair timelines remain fluid, but the consensus points to a recovery measured in months for full restoration of refining capabilities.

“We expect most attacks will not cause long-lasting disruptions. Some facilities, however, will face lengthy repair timelines.”

JPMorgan’s Natasha Kaneva

The 2026 Middle East conflict (and resulting refinery damage) has triggered a sharp rise in jet fuel prices—nearly doubling or more in many markets since late February—driving widespread aviation fare increases, fuel surcharges, ancillary fee hikes, flight cancellations, and capacity cuts.

Jet fuel now accounts for ~30-45% of many carriers’ operating costs (up from the typical 25-30%), squeezing thin margins and forcing airlines to pass costs to passengers even as a fragile U.S.-Iran ceasefire holds. While crude prices have eased slightly, refined jet fuel supply lags due to damaged Gulf refineries (as detailed previously), keeping prices elevated into the summer travel season.

Scale of Fare and Cost Impacts

- Global jet fuel price surge: Global average hit ~$209/barrel in early April 2026 (+132% year-over-year; +13.7% month-over-month). U.S. Jet A prices jumped nearly 20% in March alone; some regions saw 56-134% increases depending on location.

- Airfare increases:

- http://www.thehill.comU.S. domestic/summer fares up ~10% (per Hopper data); overall tickets +24% year-over-year in mid-March data.

- International/long-haul routes seeing steeper hikes (e.g., Asia-Europe, transatlantic affected by rerouting and supply issues).

- Airlines warn of further rises: It often takes 2-3 months for full fuel-cost pass-through into fares.

- Fuel surcharges and ancillary fees: Common response to avoid broad base-fare backlash.

- Delta: Checked bag fees +$10 (first/second) to +$50 (third); expects +$2B fuel hit in Q2 alone.

- United, American, Southwest, JetBlue: Similar bag fee increases.

- Air France-KLM: +50 euros (~$58) round-trip on long-haul.

- Cathay Pacific: Fuel surcharge +34% (up to ~$200 long-haul).

- Thai Airways: Fares +10-15%.

- Pakistan International: Domestic +$20; international up to +$100.

- WestJet: C$60 (~$43) fuel surcharge on some bookings.

- Others (Qantas, SAS, Air NZ, Kenya’s Safarilink): Direct fare hikes or adjustments.

Operational Responses (Fewer Flights = Higher Effective Prices)Airlines are trimming capacity to match fuel availability and profitability:

- Delta: Cut ~3.5% of Q2 flights (no growth vs. prior plans); focuses on off-peak routes.

- United: ~5% schedule reduction in Q2/Q3; “tactically pruning” unprofitable flying.

- Broader: Thousands of cancellations globally (e.g., SAS ~1,000 in April; Middle East carriers tens of thousands earlier due to airspace risks); U.K./Italy refueling limits caused more disruptions.

This reduces supply, which—combined with strong underlying demand in many markets—further inflates fares, especially for peak summer travel.Regional Variations and Outlook

- Hardest hit: Europe, Asia, Middle East, and Africa routes (direct exposure to Gulf refining/shipping disruptions). Examples: Johannesburg-Cape Town returns +R2,000 (~$110+).

- U.S. carriers: More insulated but still passing on costs via fees/fares; North American domestic somewhat less volatile. spglobal.com

- IATA view (Willie Walsh): Fare hikes are “already rising” due to fuel + tight capacity. Not an “existential threat,” but summer holiday prices will stay elevated for months.

Traveler impact: Book early for flexibility; monitor for deals as some carriers hedge or absorb partial costs. Demand softening is occurring in price-sensitive segments, but premium cabins remain strong. If refinery repairs drag (as expected), fares could stay 10-20%+ higher than pre-conflict levels through Q3.

foxbaltimore.comThese adjustments help airlines offset the ~$2B+ quarterly hits (e.g., Delta’s target: recover 40-50% via pricing), but consumers are bearing the brunt through higher costs and reduced options. The situation remains fluid with the ceasefire—watch for Q2 earnings updates.