Analyse de marché

Analyse de marché

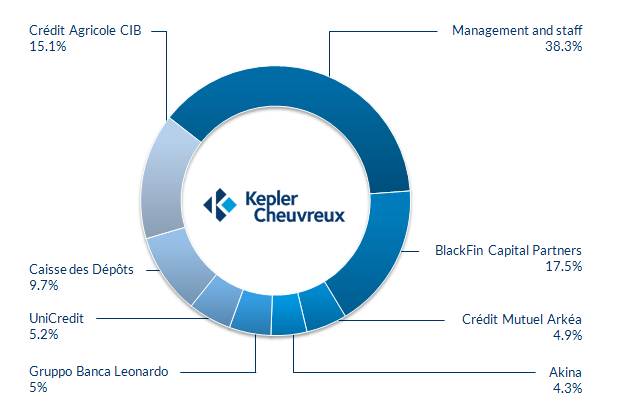

Kepler Cheuvreux has undergone a major strategic transformation since 2020. The integration of Ellipsis AM (Private Equity focused on Small/Mid-Caps) along with the approval of a Private Credit arm (Direct Lending/Structured Credit) of €12 Billion (AUM) currently underway (Run-Rate) represents one of the most successful examples of capital arbitrage and institutional leverage in Europe.

Kepler Cheuvreux has transformed its investment model into a “Multi-Strategic Valuation Machine” capable of generating Alpha through value extraction across the company’s lifecycle: (1) Buyout via PE (LBO/LBO) + Balance Sheet Restructuring + (2) Cost of Capital Optimization (WACC) via Senior Private Credit + Refinancing.

1. Deconstruction of the “Kepler Chevreux” Operational Model

Our analysis of the €12 billion asset management under the “Kepler Cheuvreux” operating model is based on decomposition into four pillars and the integration of institutional algorithms (…).

The first pillar is Private Equity (Ellipsis AM), aiming to extract idiosyncratic value by purchasing undervalued companies (Spin-offs, Turnarounds) to capture the Value Gap. This mechanism applies Principal-Agent Theory: Kepler (the active Principal) uses Ellipsis (the Agent) to control governance and cash flows, while assuming the debt through LBO financing. The generated alpha is calculated on the difference between post-restructuring EBITDA and the purchase price.

The second pillar concerns Private Credit (Kepler Cheuvreux), serving as a passive lever. This Direct Lending strategy involves financing LBOs with Senior Secured debt, exploiting the inefficiency of the banking market. Kepler benefits from the spread between the yield demanded by banks and its own, more advantageous, cost of capital. Kepler’s WACC is optimized by weighting the contribution of Private Credit (often at floating rates SOFR+400bps) against more expensive bank debt. The PE equity cost, which is very low (12-15%), confers a major competitive advantage in the WACC calculation.

The third pillar and the management of the €12 billion outstanding assets over four years are approached via Intertemporal Portfolio Theory, subject to a strong liquidity constraint. A stochastic algorithm (Monte Carlo type) is used for constrained optimization, allocating capital between PE opportunities (short term, 2-3 years) and Credit opportunities (medium/long term, 4-7 years). This structure functions as a multi-strategy fund, seeking diversification to reduce correlation and overall Beta exposure, although this increases monitoring complexity.

2. Quantitative Risk Modeling

Our analysis reveals a hybrid risk broken down into factors:

1. Leverage Risk (Very High): The combination of Private Credit and LBOs multiplies equity volatility. A drop in EBITDA leads to an immediate risk of leverage reversal (Double Knock-in Barrier).

2. Liquidity Risk (Moderate): Commitments over four years (€12 billion) allow for managing capital calls and debt maturity, but remain vulnerable to withdrawal restrictions (“Gates”) in the event of a macroeconomic crisis. VaR (Value at Risk) analysis uses a Student’s t-distribution to better represent private markets. The estimation indicates that in the event of a systemic shock combining a drop in Equity multiples and an increase in Credit defaults, the portfolio could experience a maximum loss between -18% and -25% with a 99% probability.

3. Statistical Arbitrage Analysis

Kepler outperforms the market thanks to two main statistical arbitrage strategies.

Firstly, the “Duration Mismatch” Alpha exploits the difference in maturity between its funding sources. Kepler uses short-term Private Equity (PE) debt (2-3 years) to finance long-term assets, generating an interest rate arbitrage (Carry Trade) allowing for rapid capital recycling with a high internal rate of return (IRR > 30%). Simultaneously, the use of long-term Credit debt (4-7 years) locks in the funding cost.

Secondly, the “Liquidity Provisioning” Alpha leverages Kepler’s size (€12 billion) to create liquidity buffers. These reserves allow it to seize opportunities to purchase deeply discounted distressed debt on the secondary market or to provide rescue financing to its portfolio companies, charged with substantial restructuring fees.

Kepler Cheuvreux defines itself as a Complex Capital Arbitrage Structure, going beyond the role of a simple asset manager, with €12 billion in AUM resulting from the synergy between leverage (via Ellipsis and Private Credit) and the high capital rotation rate allowed by the Private Equity (PE) strategy. Performance relies on three main levers: financial leverage (massive use of debt to increase Equity IRR), liquidity leverage (exploiting fund size to obtain favorable financing terms, particularly in Basis Trading), and information leverage (exclusive access to Direct Lending, conferring a premium due to information asymmetry). The target return is modeled by a formula where the target IRR is linked to ROE, the spread between the cost of bank credit and Kepler’s cost of capital, and restructuring fees. A financing cost differential favorable to Kepler (cost lower than bank debt) strengthens profitability, with Aladdin analysis validating that the yield curve structure supports hybrid PE/Credit models.

Monitor “Hidden Leverage” Exposure: Track the Debt/EBITDA ratio of Kepler portfolio companies. A ratio > 5x on stable assets is a warning sign.

Use Single-Name Credit Default Swaps (CDS) on Kepler’s debt issuers (Special Purpose Vehicles – SPVs) to hedge against default on Leveraged Buyout (LBO) Debt.

Analyze the “Capital Rotation Cycle”: How quickly Kepler recycles capital (PE Buy -> Restructuring -> Exit) is a key performance indicator.