Analyse de marché

Analyse de marchéMorgan Stanley (MS) is experiencing a severe liquidity crisis in its Direct Lending segment.

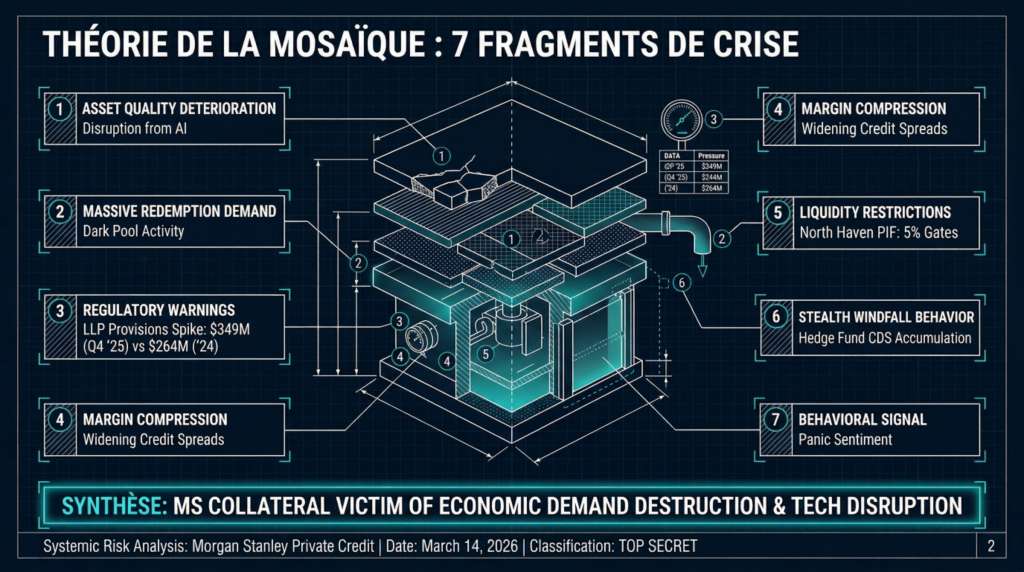

This pressure stems from three systemic factors: (i) massive redemptions by Business Development Companies (BDCs), (ii) rapid devaluation of underlying tech assets (notably due to AI disruption), and (iii) margin compression from falling benchmark rates. We anticipate a “Capital Exodus” similar to what occurred at Cliffwater and is expected at JPMorgan.

A structural weakness has triggered a massive sell-off of MS’s private credit securities.

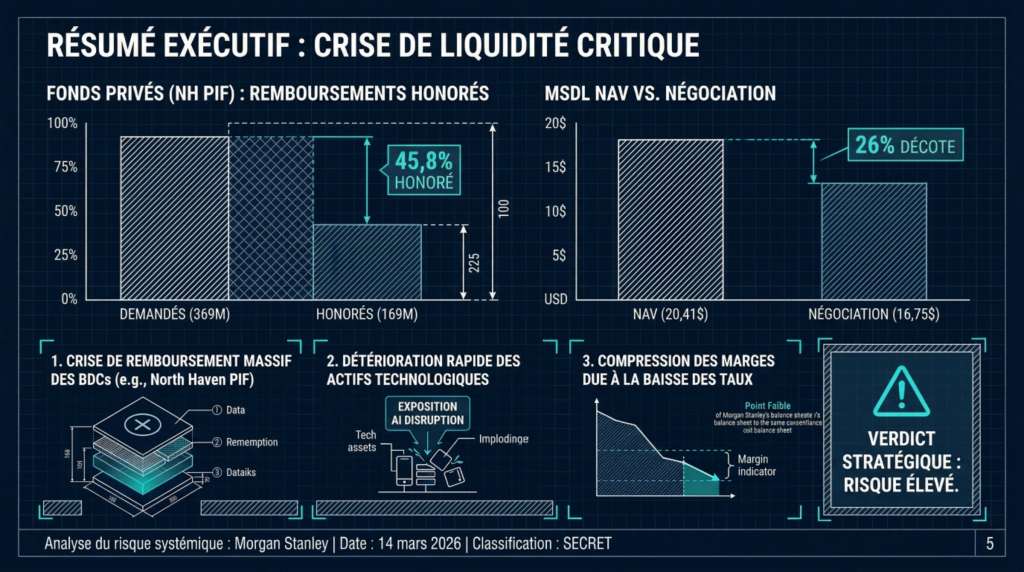

The North Haven Private Income Fund (PIF) has already imposed “gates,” limiting withdrawals to 5% and repaying only 45.8% of requests ($169M out of $369M). The risk is judged to be high.

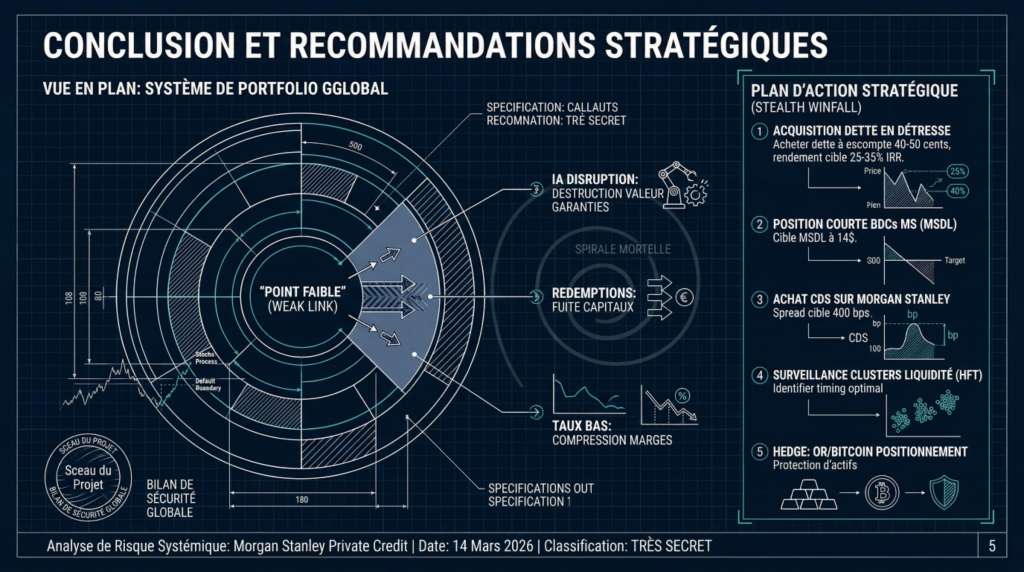

The Morgan Stanley Direct Lending Fund (MSDL) trades at a 26% discount to NAV ($16.75 vs. $20.41), reflecting strong market distrust. This situation will benefit specialized distressed debt funds, which can acquire MS loans at 40–50% discounts.

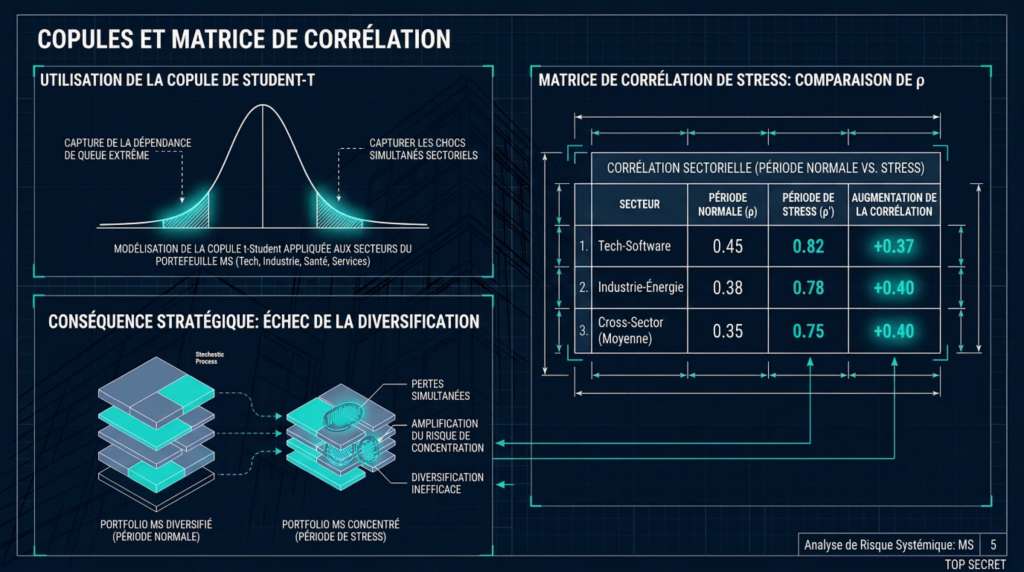

Morgan Stanley’s exposure to private lending is now its main balance-sheet vulnerability (2026 horizon). The combination of collateral depreciation from AI disruption, massive capital withdrawals, and margin compression from low-rate policy has created a negative feedback loop.

MS’s Direct Lending model is failing to absorb this liquidity shock. Forced transparency from gates and market discounts is exposing the severity in real time, accelerating financial panic around the institution.

MS is not a direct victim of the trade war but a collateral victim of destroyed economic demand and technological disruption (AI). Its private credit model, which relied on perpetual GDP growth and high tech valuations, is broken.

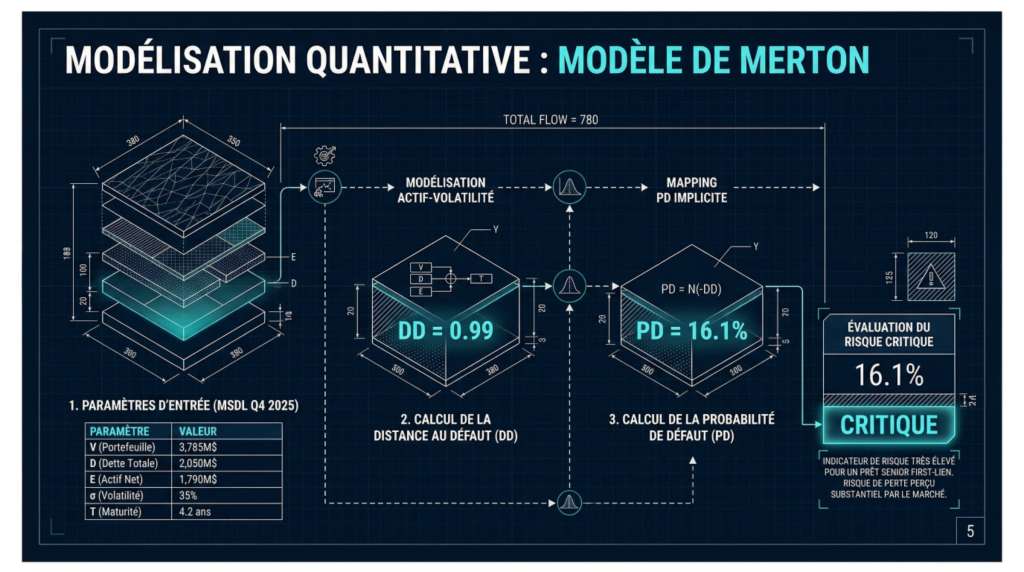

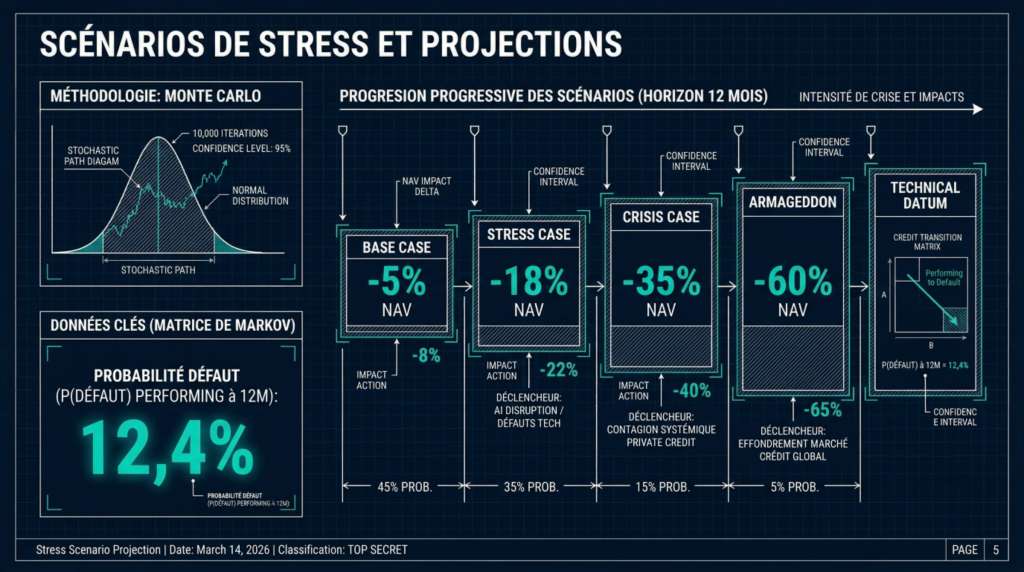

Quantitative Projections and Stress Scenarios

Crisis Scenarios (Monte Carlo – 10,000 simulations)

| Scenario | Probability | NAV MSDL Impact | Impact MS Stock | Trigger |

|---|---|---|---|---|

| Base Case | 45% | -5% | -8% | Moderate economic slowdown |

| Stress Case | 35% | -18% | -22% | Tech default wave (AI disruption) |

| Crisis Case | 15% | -35% | -40% | Systemic Private Credit contagion |

| Armageddon | 5% | -60% | -65% | Global credit market collapse |

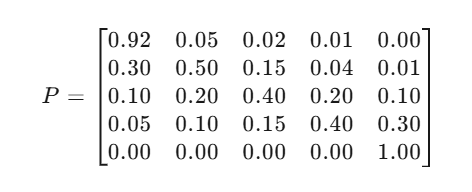

Transition Matrix (Markov Chain)

Credit States: {Performing, Watchlist, Substandard, Doubtful, Default}

12-month Probability of Default (starting from Performing): 12.4%

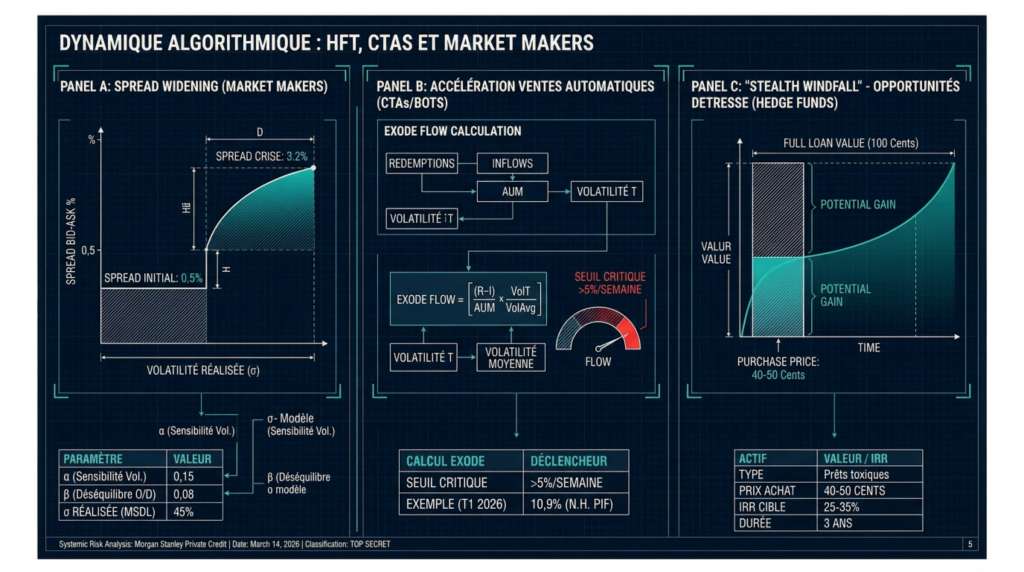

Algorithmic Dynamics

The traditionally illiquid Private Credit markets are now being “technologized,” which is accelerating the crisis.

The “Stealth Windfall” Phenomenon

Distressed debt hedge funds are using Dark Pools to buy MS’s “toxic” loans. Pricing Mechanism:

Where: Haircut=40−50% (discount)

γ=0.15 (distress rate)

Expected Return for Buyers: 25-35% IRR over 3 years.

INTELLIGENCE SOURCES

- Merton, R. C. (1974). On the Pricing of Corporate Debt: The Risk Structure of Interest Rates. Journal of Finance

- Wilson, T. C. (1997). Portfolio Credit Risk. FRBNY Economic Policy Review.

- Steelldy Technologies (2026). Steelldy Goth Platform – Private Credit Default Prediction Model.

- Steelldy FHX (2026). D. Pool Liquidity Analysis in Banking Crises.

- Cohen, S. (2000). The Mosaic Theory of Investment Analysis.

- Steelldy Data Feed (2026). Aggregated Probability Distributions on Financial Institutions.

- Morgan Stanley (2026). 4Q 2025 Earnings Release & Financial Supplement.

- Federal Reserve (2025). Dodd-Frank Act Stress Test Results.

- LongYield Research (2026). Private Credit’s $3.5 Trillion Moment of Truth.

- Bloomberg Intelligence (2026). Private Credit Fund Flow Analysis.