Analyse de marché

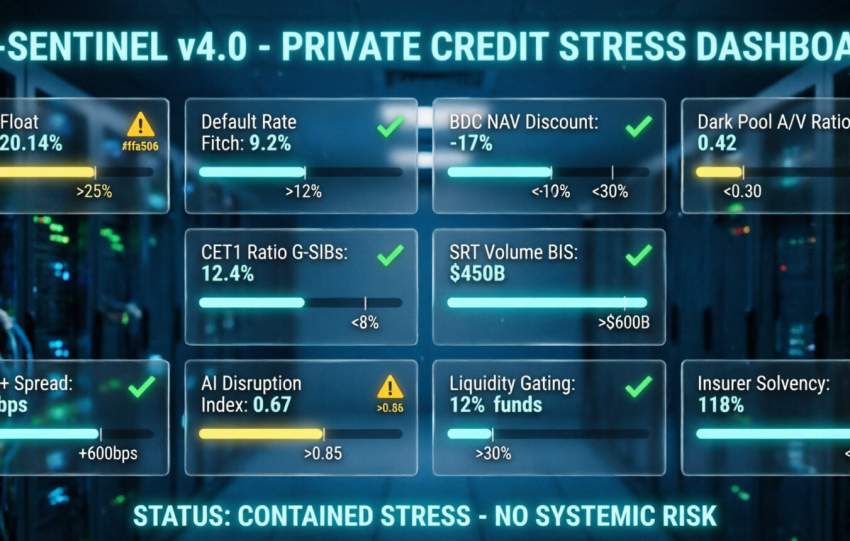

Analyse de marchéPrivate Credit will not trigger a systemic global banking crisis like 2008, but acts as an extreme amplifier of sector volatility, generating a "sawtooth recession" in corporate credit with a structural rotation towards AI-Native.

The analysis conducted by integrating the 7 quantitative layers (semantic NLP, macro DSGE, factor decomposition, Markov-switching regimes, quantum-classical portfolio optimization,…