Analyse de marché

Analyse de marchéThe Monte Carlo analysis of JPY carry trade unwind uses a Merton Jump-Diffusion model to simulate USD/JPY dynamics over a 90-day horizon, capturing both continuous exchange rate movements and sudden discontinuities from forced position closures. The model incorporates calibrated parameters including a spot rate of 158.5, stressed volatility ranging from 9% to 18%, and jump…

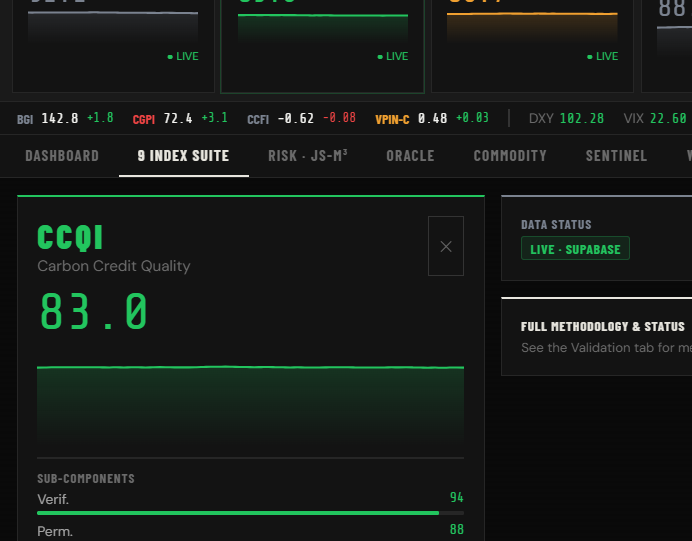

Carbon Credit Market

Carbon Credit Market