Analyse de marché

Analyse de marché

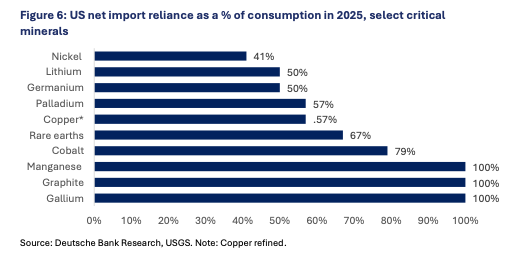

The « USGS 2025 report » refers to the U.S. Geological Survey’s Mineral Commodity Summaries 2025 (MCS 2025), the annual publication that provides the data referenced in the chart from the tweet you shared.

This 212-page report (Version 1.2, March 2025) was released on January 31, 2025 (with minor revisions in February and March). It is the primary U.S. government source for nonfuel mineral data, covering production, consumption, trade, and import reliance for more than 90 mineral commodities. The full PDF is freely available here: https://pubs.usgs.gov/periodicals/mcs2025/mcs2025.pdf.

Important note on the data year

The report presents 2024 data (with estimates where final figures were unavailable). Net import reliance is calculated as a percentage of 2024 apparent consumption. The tweet’s chart labels it as « % of 2025 Consumption » — this is likely because the report itself is titled for 2025 (a standard naming convention) or because Deutsche Bank Research applied minor forward-looking adjustments/projections. The underlying USGS figures align exactly with the tweet’s examples (e.g., graphite and gallium at 100%, cobalt at 76%).

Key Section: U.S. Net Import Reliance (Figure 2 in the Report)

The report highlights U.S. dependence on foreign sources in its « Significant Events, Trends, and Issues » overview and Figure 2 (« 2024 U.S. Net Import Reliance »). In 2024:

- Imports made up >50% of apparent consumption for 46 nonfuel mineral commodities.

- The U.S. was 100% net import reliant for 15 commodities (12 of which are on the 2022 Critical Minerals List).

- An additional 28 critical minerals (including the 14 lanthanides grouped under rare earths) had >50% net import reliance.

Here is the complete list of net import reliance percentages extracted directly from the report’s Figure 2 and supporting tables (not all 90 and commodities are shown if they were net exporters or <20% reliant):100% net import reliant:

- Arsenic (all forms)

- Asbestos

- Cesium

- Fluorspar

- Gallium (metal)

- Graphite (natural)

- Indium

- Manganese

- Mica (natural sheet)

- Niobium (columbium)

- Rubidium

- Scandium

- Strontium

- Tantalum

- Yttrium (compounds)

>95% or very high:

- Gemstones: 99%

- Abrasives (fused aluminum oxide): >95%

- Nepheline syenite: >95%

- Titanium (sponge metal): >95%

Other notable high-reliance commodities (relevant to batteries, electronics, renewables, and defense):

- Cobalt (metal, oxides, and salts): 76%

- Rare earths (compounds and metals, including 14 lanthanides): 80%

- Potash: 93%

- Bismuth: 89%

- Antimony: 85%

- Platinum: 85%

- Chromium (all forms): 77%

- Tin (refined): 73%

- Zinc (refined): 73%

- Barite: >75%

- Bauxite: >75%

- Magnesium (metal): >75%

- Germanium: >50%

- Lithium: >50%

- Tungsten: >50%

- And many others (e.g., alumina 59%, magnesium compounds 52%).

Minerals with low or zero reliance (net exporter or <20%) include abrasives (metallic), beryllium, boron, gold, helium, iron ore, molybdenum, soda ash, zinc (ores/concentrates), and construction materials like sand/gravel and crushed stone.

Leading Import Sources and China Dependency (2020–2023 averages)China remains the dominant supplier for many critical minerals. Key examples from the report:

- Graphite (natural): China 43%

- Gallium: Japan/China/Germany/Canada (China is the global primary producer at 99% and banned exports to the U.S. in Dec 2024)

- Rare earths (compounds/metals): China 70%

- Cobalt: Norway/Finland/Japan/Canada (but China dominates global refining)

- Arsenic: China 52%

- Antimony: China 63% (plus new 2024 export restrictions)

China was the leading import source for 21 of the listed commodities (tied with Canada). The report notes China’s export bans/restrictions on antimony, gallium, and germanium in late 2024, which further heighten supply risks.

pubs.usgs.govU.S. Critical Minerals UpdateThe report references the 2022 Final List of 50 Critical Minerals (which added nickel and zinc, broke out individual rare-earth elements and platinum-group metals, and removed a few others). Highlights:

- Domestic production value of critical minerals fell 24% to $3.3 billion in 2024.

- Recycling supplied ~20% of some critical mineral needs ($9.7 billion value).

- Government investments (DoD, DOE, CHIPS Act) are funding new domestic projects in graphite, lithium, cobalt, rare earths, etc.

- New facilities noted (e.g., graphite plant in Louisiana; fluorspar mine in Utah commissioning in 2025).

Over the past 20 years (see Figure 9 in the report), reliance has stayed persistently high for most critical minerals, with only minor improvements in a few cases (e.g., rare earths compounds/metals dropped from >95% in 2023 to 80% in 2024 due to domestic output growth at Mountain Pass, CA).

pubs.usgs.govAdditional Resources in the Report

- Table 5: Salient statistics for critical minerals in 2024.

- Individual 2-page commodity summaries (e.g., dedicated cobalt, gallium, graphite, rare earths sections) with 5-year trends, world production, reserves, and events/trends.

- Data release (CSV files): USGS data portal for raw numbers.

- Interactive dashboard (mentioned on the USGS page): Tableau visualization of the data.

If you want details on a specific mineral (e.g., full cobalt or rare earths chapter), 20-year trends, world production tables, or anything else from the 212-page report, let me know—I can pull exact quotes or tables from it. The report underscores the supply-chain vulnerabilities highlighted in the tweet and the push for domestic mining/processing.

China export restrictions

China’s export restrictions on critical minerals are a key driver of the U.S. net import reliance highlighted in the USGS Mineral Commodity Summaries 2025 and the Deutsche Bank chart you referenced (e.g., 100% reliance on imports for graphite and gallium, high reliance for rare earths, antimony, etc.). Beijing uses licensing requirements, end-use/end-user checks, and occasional outright bans (often framed as dual-use or national security measures) to control exports of these materials, where it dominates global production and refining.These controls have escalated since 2023 in response to U.S. semiconductor and tech restrictions, but many U.S.-targeted measures were suspended in November 2025 following U.S.-China trade negotiations under the Trump administration. As of March 31, 2026, the suspensions remain in effect until November 2026, though the underlying legal framework is intact and earlier (non-U.S.-specific) controls continue. Re-imposition is possible if tensions rise again.

Key Timeline of Restrictions (2023–2026)

- 2023: Initial dual-use export licensing on gallium and germanium (August); graphite forms added later.

- September 2024: Antimony added to export controls.

- December 3, 2024 (MOFCOM Announcement No. 46): U.S.-specific tightening — “In principle, exports of dual-use items related to gallium, germanium, antimony, and superhard materials to the United States shall not be permitted.” Stricter end-user/end-use reviews for dual-use graphite to the U.S. cset.georgetown.edu

- February 2025: New licensing on tungsten, tellurium, bismuth, indium, and molybdenum.

- April 4, 2025 (MOFCOM Announcement No. 18): Export controls on seven medium/heavy rare earth elements (samarium, gadolinium, terbium, dysprosium, lutetium, scandium, yttrium) plus related compounds, metals, and magnets. Licensing required with end-user disclosure. english.mofcom.gov.cn

- October 9, 2025: Major expansion (Announcements 55–62) — Added five more rare earths (holmium, erbium, thulium, europium, ytterbium); controls on rare earth processing equipment/technologies; lithium-ion battery supply chain items. Extraterritorial reach: licenses needed even for foreign-made magnets/products with trace (≥0.1%) Chinese-origin rare earths or using Chinese tech. Military-affiliated buyers largely denied licenses.

November 2025 suspensions (post U.S.-China deal):

- October 2025 rare earth/magnet/battery controls suspended until November 10, 2026.

- Article 2 of the December 2024 U.S.-specific ban (gallium, germanium, antimony, superhard materials) suspended until November 27, 2026 — exports now handled under standard (non-ban) licensing.

- Stricter U.S.-specific graphite reviews also paused.

General licenses were issued for U.S. end-users in some cases. April 2025 rare earth controls were not suspended.

Current Status (as of March 31, 2026) for Minerals in the USGS/Tweet ContextAll restrictions below still require export licenses in most cases (with potential delays, denials, or end-use scrutiny). There are no active outright bans on exports to the U.S. for the key minerals due to the 2025 suspensions, but the system remains selective and opaque.

| Mineral (USGS 2024 Reliance) | China’s Global Role | Current Export Controls (March 2026) | U.S. Impact Notes |

|---|---|---|---|

| Gallium (100%) | ~99% of global production | Standard licensing (U.S.-specific ban suspended Nov 2025) | Key for semiconductors/defense; prior 2023–2024 controls already disrupted supply chains. |

| Graphite (natural) (100%) | ~43% of U.S. imports; dominant refiner | Dual-use graphite under standard licensing (U.S.-specific stricter reviews suspended) | Critical for EV batteries; high-purity forms remain sensitive. |

| Rare Earths (80% for compounds/metals) | 60–70% production; 90% refining | April 2025 licensing on 7 heavy REEs + compounds/metals/magnets still active; October expansions suspended | Affects magnets for EVs, wind turbines, defense. Extraterritorial rules paused but framework exists. |

| Antimony (85%) | 48–63% global/U.S. imports | Standard licensing (U.S.-specific ban suspended Nov 2025) | Used in flame retardants, ammunition, batteries; prices spiked during 2024 restrictions. |

| Germanium (high reliance) | Dominant producer | Standard licensing (U.S.-specific ban suspended) | Semiconductors, optics, solar; often paired with gallium controls. |

| Cobalt (76%) | Dominant refiner (not primary miner) | No new specific 2024–2025 controls; general oversight | China processes most global cobalt; indirect leverage via refining dominance. |

Other 2025 additions (tungsten, bismuth, indium, etc.) remain under licensing but are less central to the tweet’s chart.

Broader Context and Outlook

- Licensing reality: Even under “standard” rules, exporters must disclose end-users and uses; approvals can be slow or denied for sensitive applications (e.g., military). China has used this selectively.

- U.S. vulnerabilities: These restrictions directly amplify the risks in Figure 2 of the USGS 2025 report (46 commodities >50% import reliant). USGS modeling (2024) estimated a full gallium/germanium ban could cost the U.S. ~$3.4 billion in GDP.

- Suspensions are temporary: They expire in November 2026 and were part of a broader U.S.-China trade truce. A February 2026 metals industry briefing signaled ongoing tightening/oversight of rare earth exports.

- Diversification push: The controls have accelerated U.S./allied efforts (e.g., domestic graphite plants, rare earth processing, recycling) noted in the USGS report.

Critical minerals geopolitics in 2026

Critical minerals geopolitics in 2026 centers on a high-stakes global contest for control of supply chains essential to defense, EVs, renewables, semiconductors, and advanced manufacturing. These materials (e.g., graphite, gallium, rare earth elements/REEs, cobalt, lithium, antimony) are no longer just commodities—they are strategic assets in great-power competition, primarily between the US-led bloc and China.

This dynamic directly amplifies the US vulnerabilities outlined in the USGS Mineral Commodity Summaries 2025/2026 (e.g., 100% net import reliance for graphite and gallium, high reliance for cobalt and REEs) and the Deutsche Bank chart from the original tweet. China’s processing dominance (often 50–99% globally) gives it leverage to weaponize exports, while the US and allies are accelerating “friend-shoring,” domestic scaling, and plurilateral alliances to de-risk.

China’s Dominant Position and Strategic Leverage

China controls the majority of global mining, refining, and downstream processing for many critical minerals, turning them into tools of economic coercion:

- Production/Refining Monopoly: ~99% of gallium, dominant in graphite refining, 60–90% of REEs (especially heavy REEs), and major shares in cobalt refining and antimony.

- Export Controls as Geopolitical Tool: Licensing regimes (escalated 2023–2025) targeted dual-use items. Key 2025 measures (e.g., on heavy REEs in April; broader October expansions on magnets, processing tech, and extraterritorial rules) were suspended in November 2025 under the US-China trade truce until November 2026. Standard licensing and oversight remain, with industry briefings in March 2026 signaling potential tightening. Reimposition risks remain high if tensions escalate.

- Resource Nationalism: Beijing restricts raw ore exports to capture value domestically and invests heavily in Global South projects (Africa for cobalt, Latin America for lithium).

This concentration creates “chokepoints” that can spike prices or disrupt defense/tech supply chains overnight.

US-Led Diversification and Alliances

The Trump administration has reframed critical minerals as a core national security imperative (shifting emphasis from climate goals), deploying executive actions, massive financing (~$30B+ in recent loans/grants), and diplomacy:

- FORGE (Forum on Resource Geostrategic Engagement): Launched February 4, 2026, at the Critical Minerals Ministerial (54 countries + EU). Successor to the Minerals Security Partnership (MSP). Focuses on project-level investments, policy coordination, and a proposed preferential trading bloc with price floors to counter Chinese dumping. Chaired initially by South Korea (until June 2026). Aims for “bold and decisive action” on resilient chains.

- Bilateral Surge: 13+ new MOUs/frameworks signed in early 2026 (e.g., Australia, DRC, Japan, Brazil). Complements Pax Silica (tech supply chains) and Project Vault (major domestic stockpile).

- Domestic/Industrial Policy: Executive orders streamline permitting; DOE/DoD/EXIM funding for graphite, lithium, REEs, gallium recovery; antidumping duties on Chinese imports.

This plurilateral approach seeks scale that bilateral deals alone can’t deliver, while avoiding over-reliance on any single partner.

Other Key Players and Emerging Alliances

- European Union: Critical Raw Materials Act drives “strategic autonomy.” New EU-Australia trade deal (signed March 2026) removes 99%+ tariffs on critical minerals (lithium, aluminum, manganese) to stabilize chains and hedge China. EU also pushes trilateral deals (e.g., with India/Australia in Africa). reuters.com

- Australia: Major producer (lithium, REEs) and key US/EU partner. Benefits from tariff-free access and “buyers club” discussions.

- Global South as Battleground: US/China rivalry plays out in Africa (DRC cobalt), Latin America (lithium “triangle”), and Asia. Resource nationalism rises—countries demand local processing/value capture. Potential India-Australia-Africa trilateral for diversified chains. blogs.lse.ac.uk

- Others: Japan/South Korea as tech consumers; Canada risks deeper US dependence; deep-sea mining gains traction in US strategy (EEZ focus, international partnerships).

Key Geopolitical Risks and Flashpoints (2026)

| Risk/Flashpoint | Description | Potential Impact |

|---|---|---|

| Suspension Expiry (Nov 2026) | China’s controls on REEs, gallium, etc., could snap back. | Immediate price spikes, defense/tech disruptions. |

| Global South Competition | China’s existing investments vs. Western financing. | Delayed diversification; new dependencies. |

| Price/Trade Wars | Proposed Western price floors vs. Chinese dumping. | Market distortion; M&A surge in mining. |

| New Dependencies | Shift from China to US-led blocs (e.g., Canada). | Reduced resilience if alliances fracture. |

| Deep-Sea/Environmental | US push for seabed minerals amid ISA debates. | Legal/geopolitical tensions; local opposition. |

Overall, 2026 marks consolidation of politicized supply chains: policy support, M&A, and alliances are driving diversification, but full decoupling from China will take years. Non-Chinese capacity is growing (e.g., US REE output up), yet vulnerabilities persist.

Sources

1. https://www.reuters.com/world/china/china-suspends-ban-exports-gallium-germanium-antimony-us-2025-11-09/