Analyse de marché

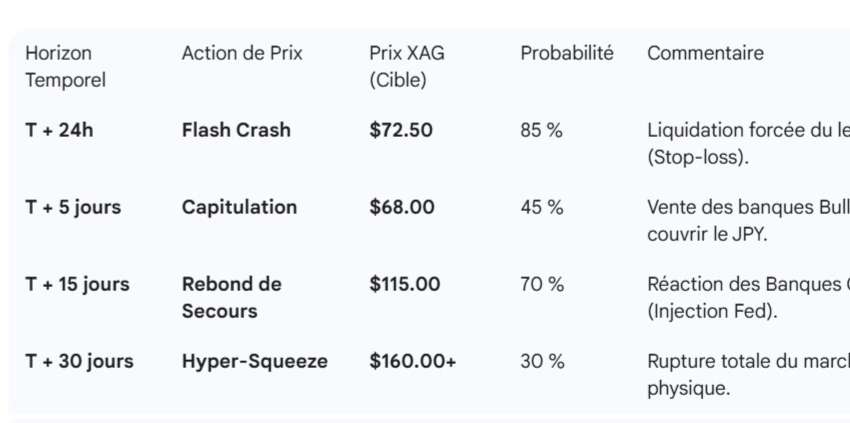

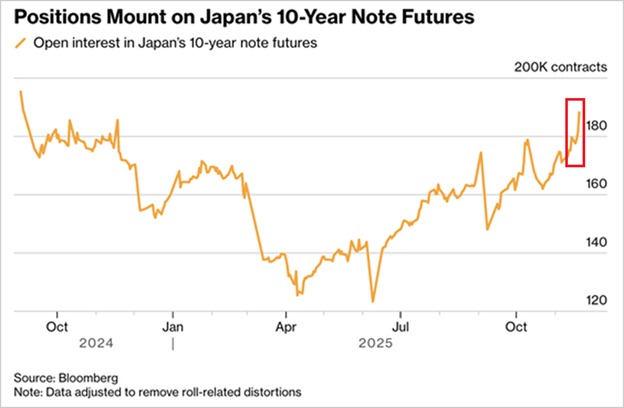

Analyse de marché1. SYNTHÈSE DU RISQUE DE LA « CRISE DE LIQUIDITÉ » INITIALE CONTRE REBOND SYSTÉMIQUE Le dénouement du Carry Trade JPY représente le risque extrême le plus brutal pour le premier trimestre 2026. Si le croisement USD/JPY dépasse le niveau psychologique de 145, nous prévoyons une vente forcée des actifs à haut bêta. En ce…